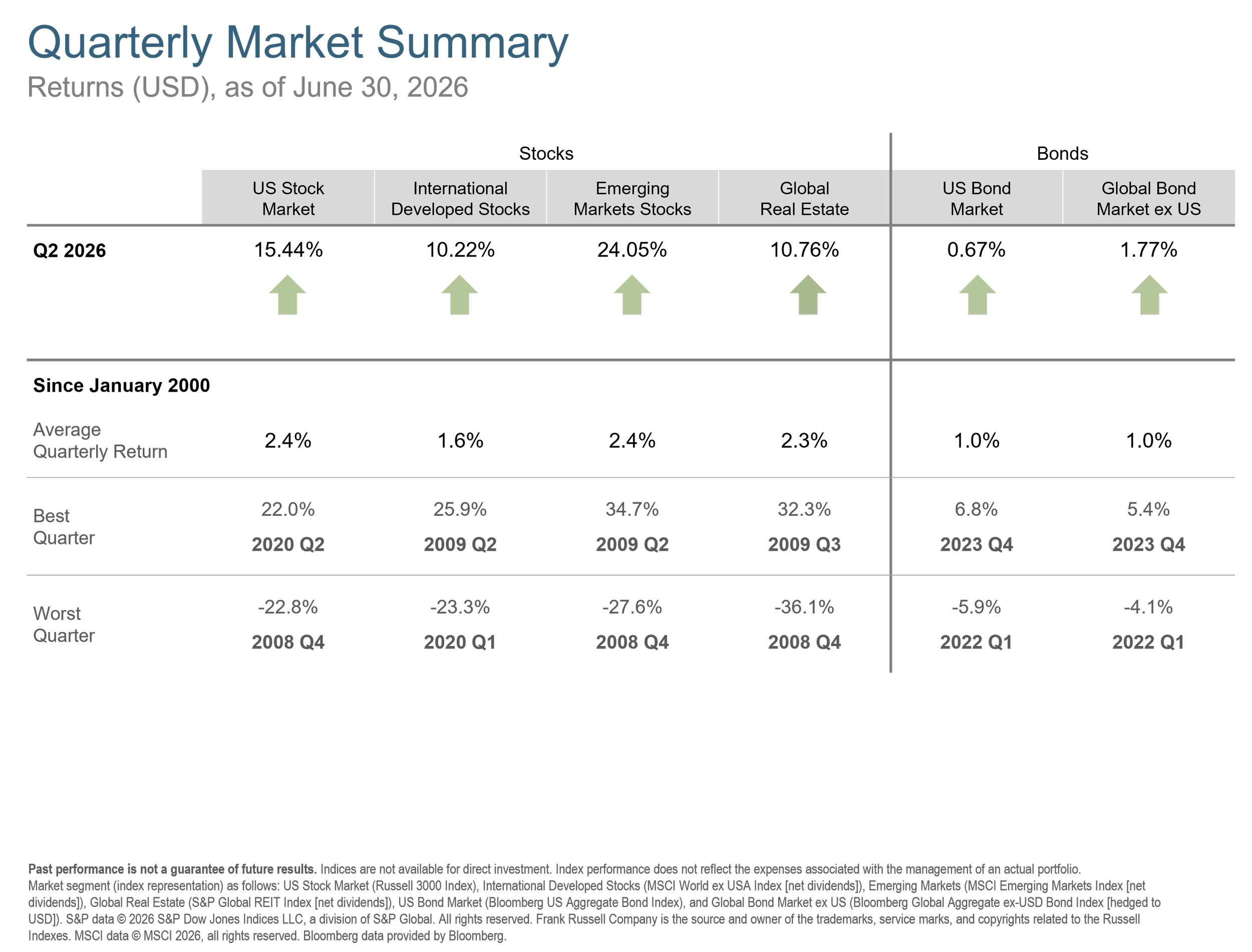

If someone had offered investors a quarter in which U.S. stocks gained more than 15%, developed international stocks gained 10%, emerging markets gained 24%, real estate gained nearly 11%, and bonds remained positive, most would have accepted. They probably would not have ordered war in the Middle East, violent oil-price swings, stubborn inflation, rising Treasury yields, and one of the S&P 500's worst days in three decades as the delivery method. Markets rarely ask how we would prefer our returns to arrive.

After stumbling in March, global stocks rallied sharply through the second quarter. The Russell 3000 Index gained 15.44% for the quarter and finished the first half up 10.88%. Developed international stocks rose 10.22% in Q2, while emerging markets led with a 24.05% return. Even the broad U.S. bond market, which faced higher Treasury yields, produced a modest 0.67% gain.

Those are excellent numbers. They are also a useful reminder that a good return does not have to feel good while it is happening. Investors were asked to absorb daily headlines that could easily have supported a decision to reduce risk. The market rewarded patience anyway, though there was no way to know that in advance.

Diversification stopped feeling decorative

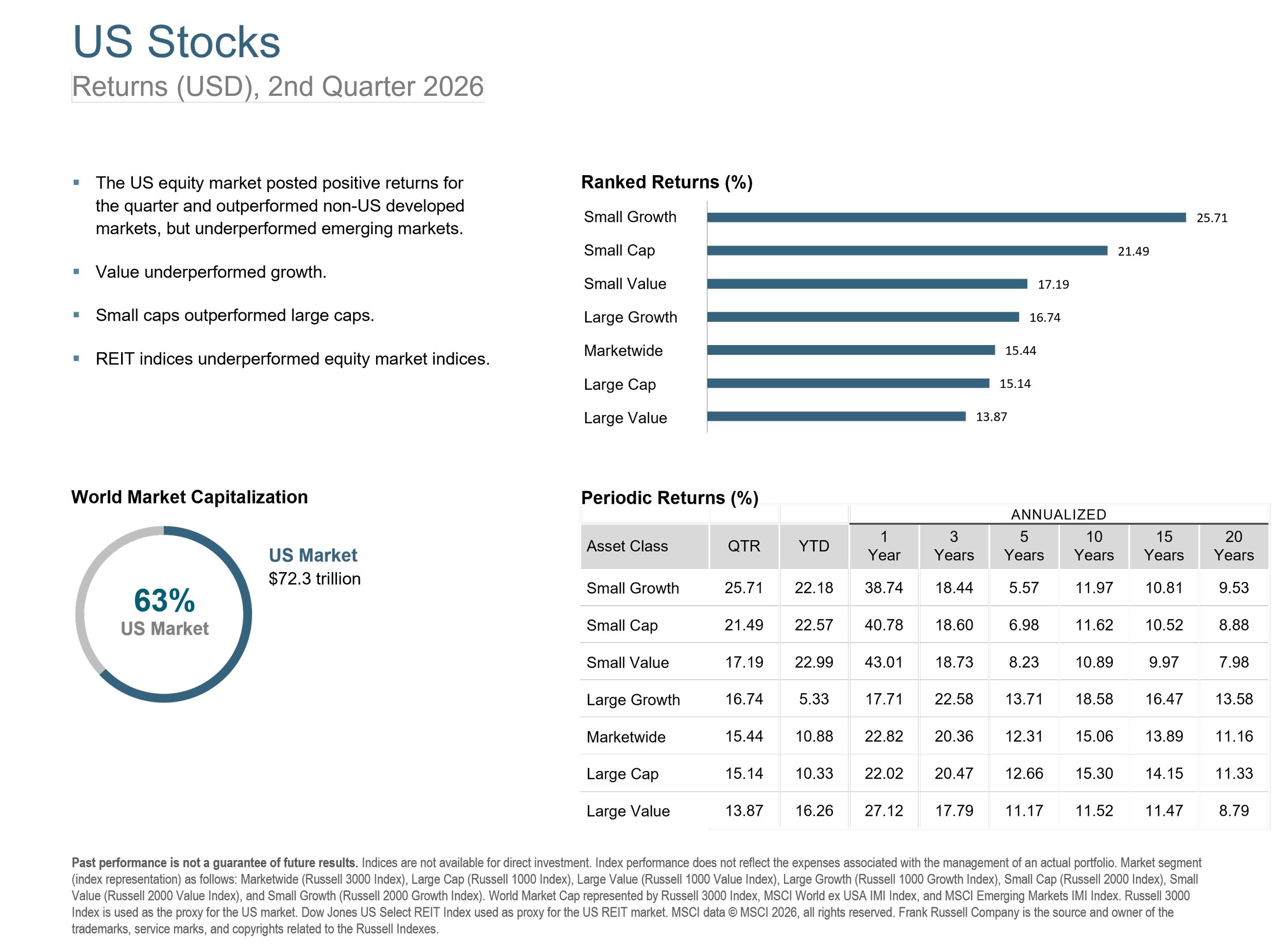

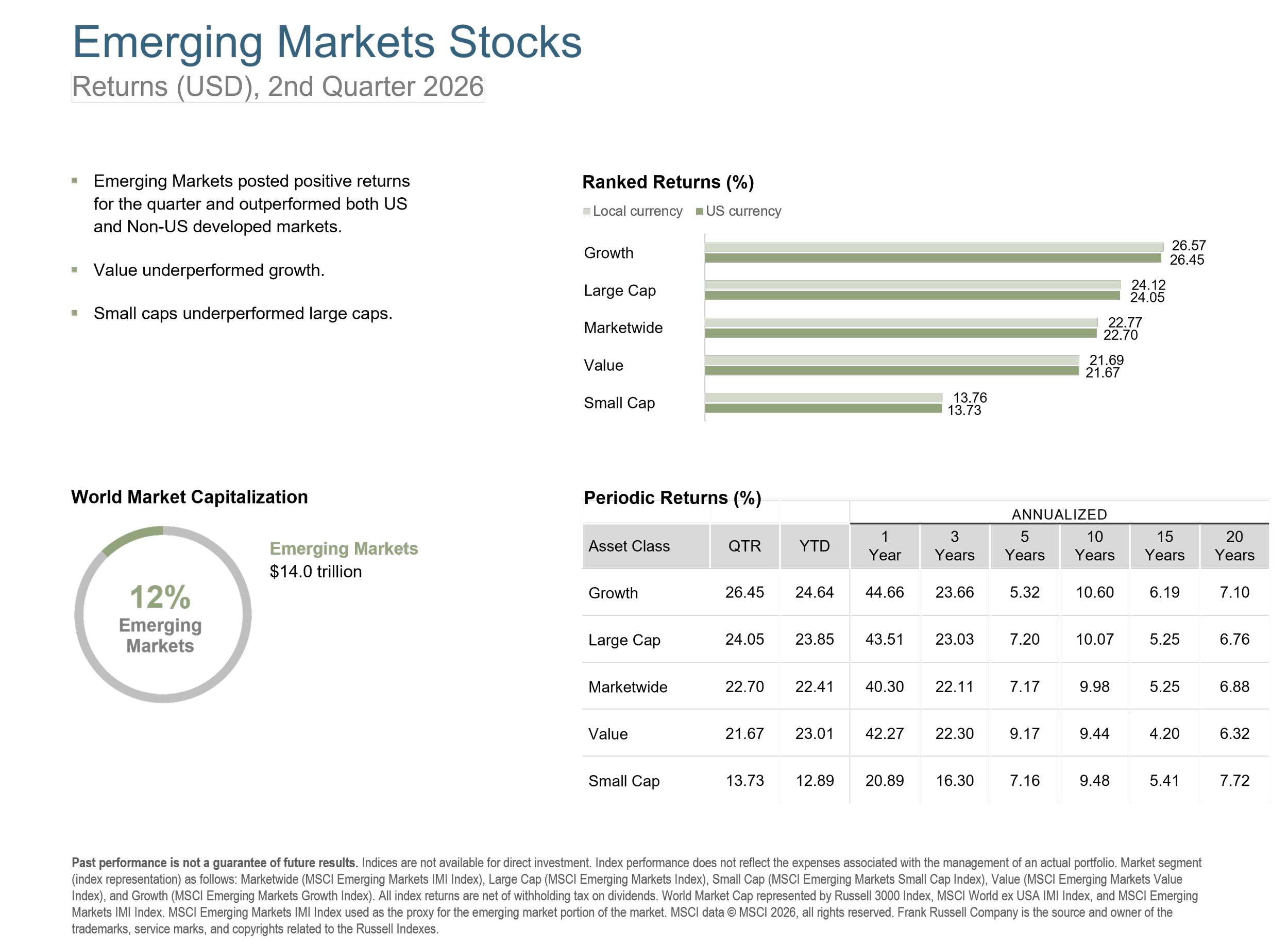

The United States represents about 63% of the global stock market, which is enormous, but it is not 100%. During Q2, the other 37% mattered. Emerging markets outpaced both the United States and developed international markets. A portfolio concentrated only in the recent U.S. winners would have missed a meaningful part of the quarter's return.

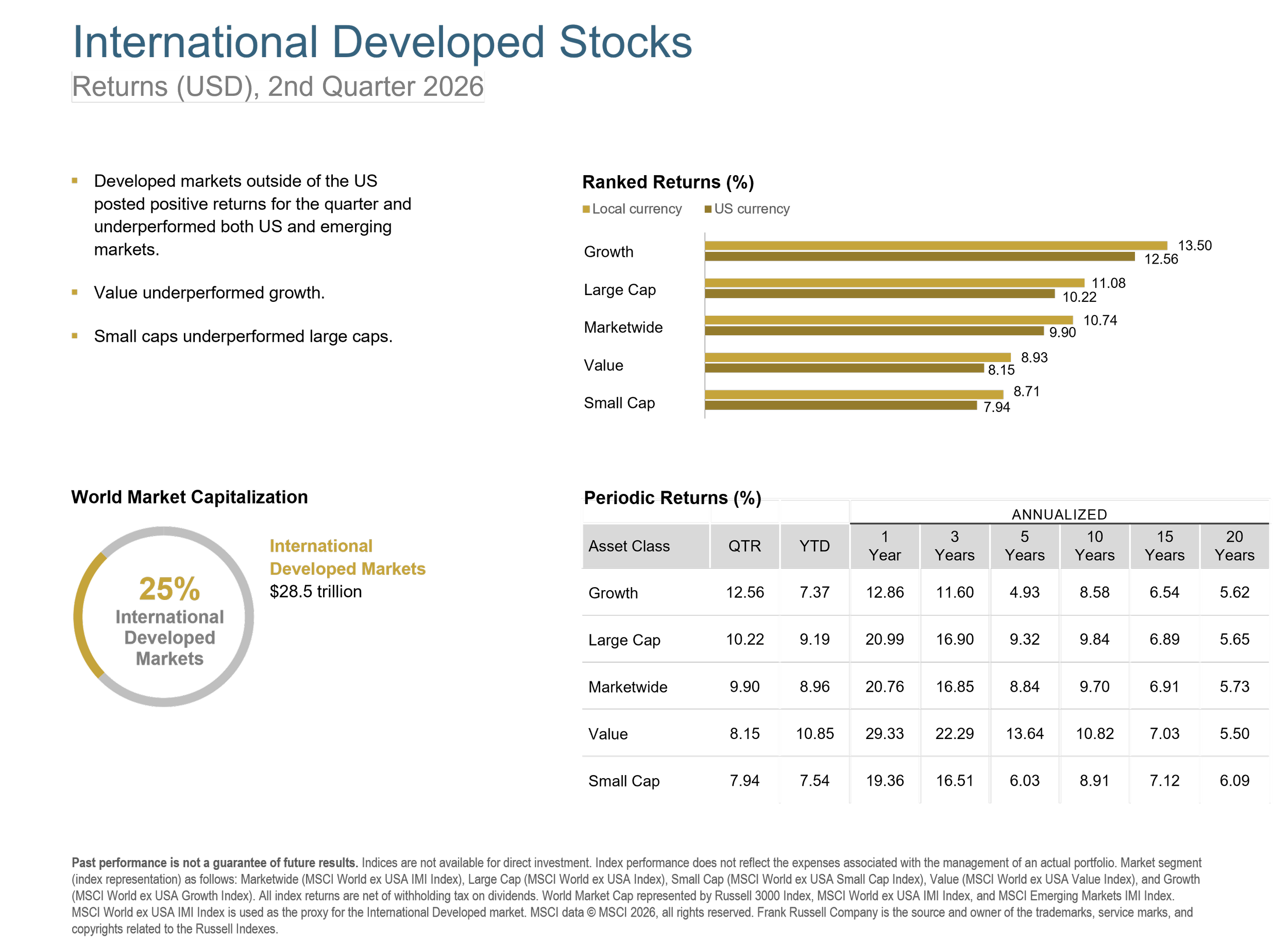

Leadership also changed depending on the period measured. U.S. small-cap growth led in Q2 with a 25.71% return. Over the full first half, however, small value gained 22.99% and large value gained 16.26%, while large growth gained just 5.33%. International growth outperformed value during the quarter, but value remained ahead in the first half. Simple sometimes ain't so simple.

The lesson is not that investors should now chase emerging markets, small growth, or value. The lesson is that different parts of a diversified portfolio should behave differently. If every holding acts like the S&P 500, the portfolio may be diversified in name only. Tracking error can be uncomfortable, but it is often evidence that diversification is actually present.

Exhibit 1. US Stocks

Exhibit 2. International Developed Stocks

Exhibit 3. Emerging Markets Stocks

Rates and inflation sent mixed signals

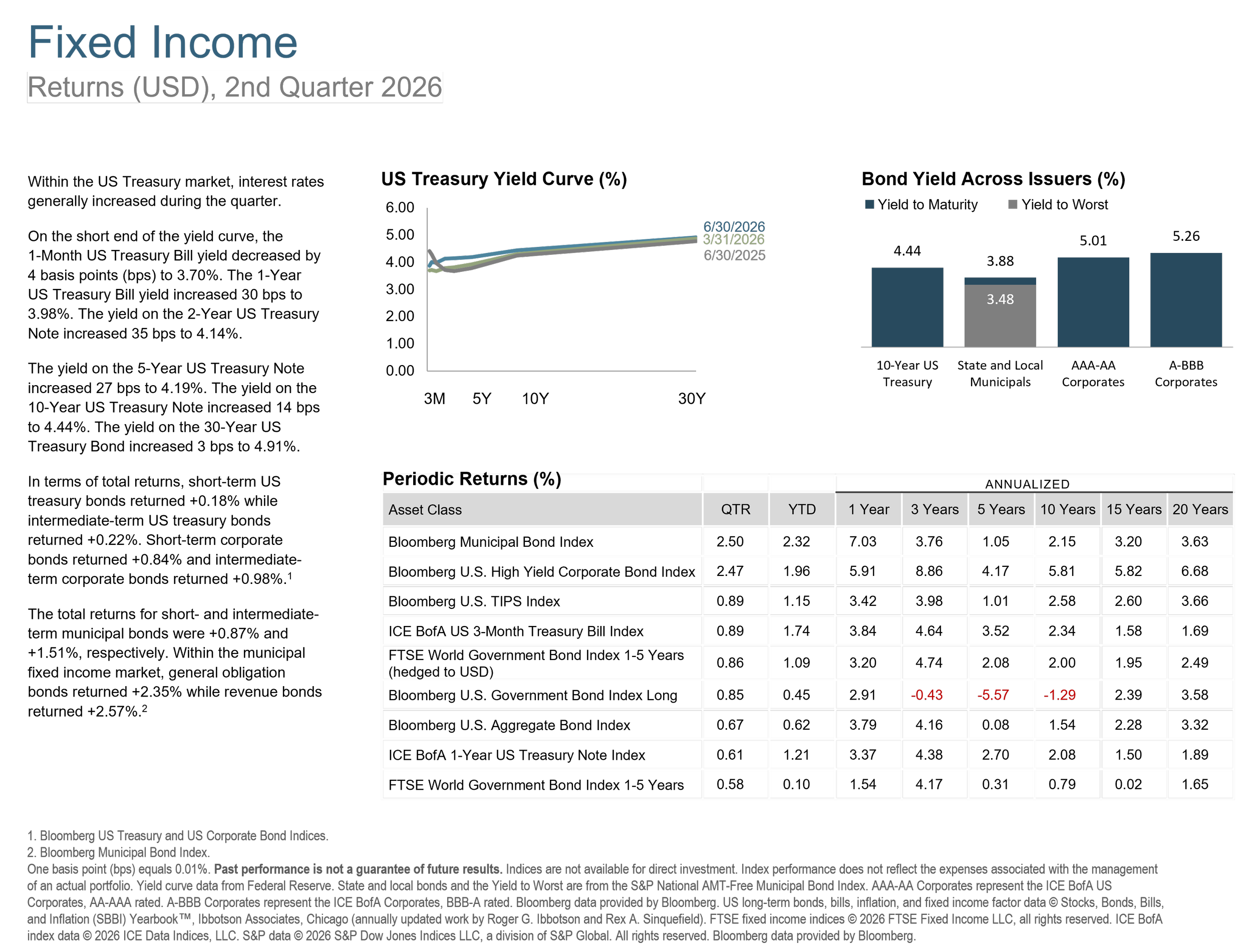

The Federal Reserve kept its target rate at 3.50% to 3.75% in June. Meanwhile, the 10-year Treasury yield rose from 4.30% at the end of March to 4.44% on June 30. Rising yields generally pressure bond prices, but coupon income helped the broad bond market remain positive. Bonds are not a single trade, and a modest increase in rates does not automatically lead to a negative total return.

Inflation was more complicated. Headline CPI rose 4.2% over the 12 months ending in May, influenced heavily by energy. Data released after the quarter end showed headline inflation easing to 3.5% in June and core inflation slowing to 2.6%. That is encouraging, but one month does not settle the argument. Energy prices can reverse quickly, and the Fed's decisions will continue to depend on the incoming data rather than anyone's preferred forecast.

Exhibit 4. Fixed Income

The crisis hedge did not read the script

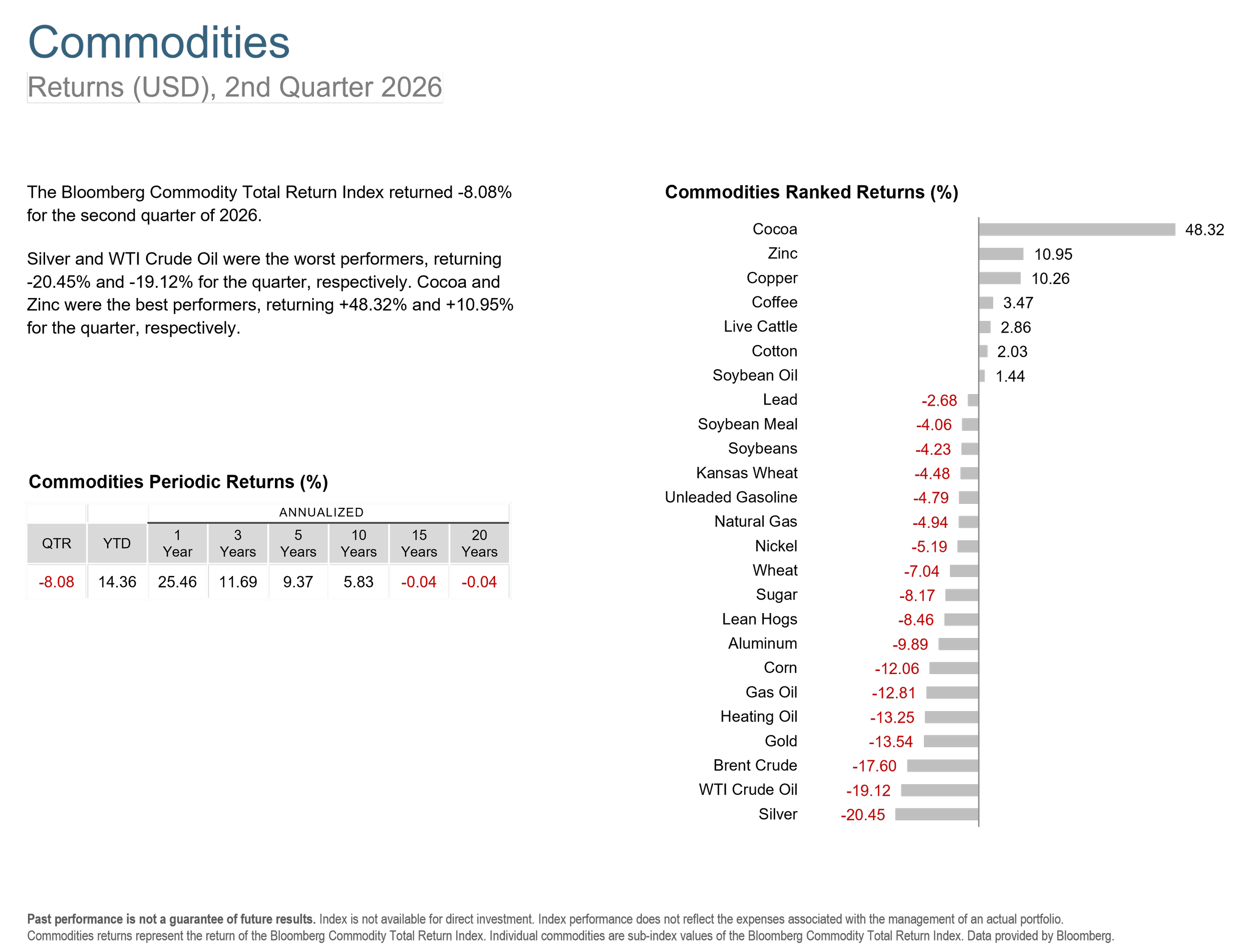

Geopolitical conflict and inflation are often presented as ideal conditions for commodities and precious metals. Yet the Bloomberg Commodity Total Return Index fell 8.08% in Q2. Gold lost 13.54%, WTI crude oil lost 19.12%, and silver lost 20.45%. Commodities still finished the first half up 14.36%, so the point is not that they never work.

The better point is that labels such as inflation hedge or crisis hedge can create false confidence. An asset can help in some environments and disappoint in others that appear tailor-made for it. I would rather assign every holding a deliberate portfolio role than rely on a story about what it is supposed to do.

Exhibit 5. Commodities

Alternatives: different return engines, different measurements

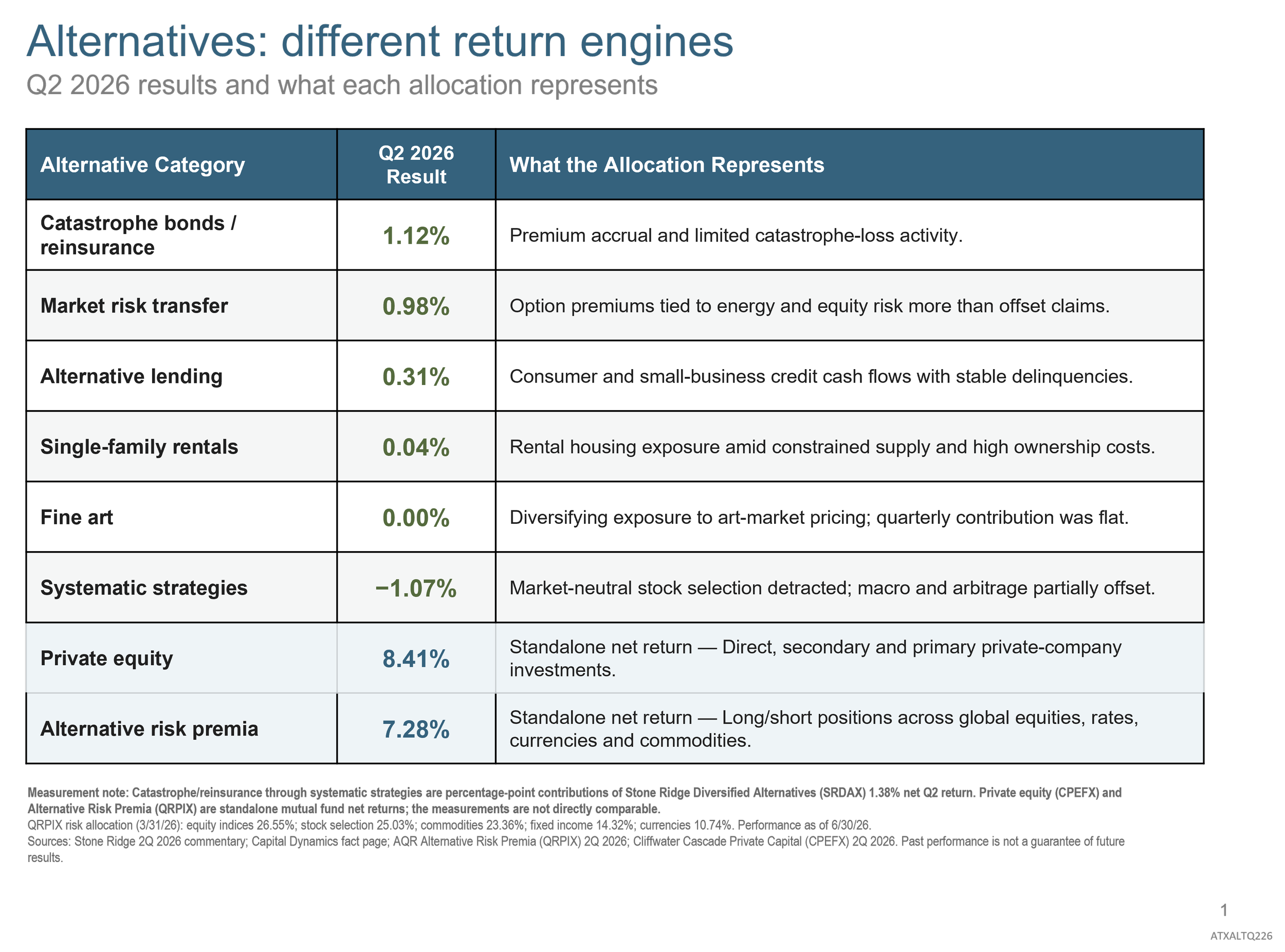

Alternative investments are sometimes discussed as though they were a single asset class. They are not. During Q2, the strategies represented in our portfolios produced a wide range of results for different reasons. The following table shows how individual strategies contributed to the return of a diversified alternatives portfolio. These are contribution figures, not standalone asset-class returns.

Exhibit 6. Alternatives

What I would do with this quarter

A strong quarter can tempt investors into bad decisions just as easily as a weak one. Chasing is chasing, whether the recent winner is a U.S. technology stock, an emerging market, a commodity, or an alternative strategy. I would use the quarter as a reason to do the quieter work:

Rebalance portfolios that have moved materially away from their intended allocation.

Review near-term spending reserves so market risk is not carrying a job it was never meant to carry.

Evaluate positions by their role, risks, costs, and liquidity, not only by the latest return.

Update financial-plan assumptions if spending, taxes, or cash needs have changed.

I would not read too much into one quarter, even a very good one. The durable lesson is that markets can reward investors while the news remains unsettling, leadership can shift without warning, and a well-built portfolio should not depend on correctly predicting the next headline.

If your allocation has drifted, your cash needs have changed, or you would like a second opinion on how the pieces fit together, get in touch through the ATX Portfolio Advisors contact page. A disciplined review is usually more useful than another forecast.