When I ask someone about their best trade, I frequently hear a pretty good story.

Someone bought Apple years ago. Someone bought Nvidia before artificial intelligence became the only thing anyone on financial television wanted to talk about. Someone sold a stock right before it collapsed. Someone bought back into the market near the bottom in 2020 and now remembers it as if they were staring down the bear market with ice water in their veins.

Maybe they were. Or maybe they got lucky.

That is why I think the better question is not, “What was your best trade?” The better question is, “What was your luckiest trade?”

The distinction matters. A good outcome does not always mean there was a good process behind it. Anyone who has played golf, poker, or watched enough sports should understand that concept quite well. Occasionally the result looks brilliant on the scoreboard, but the decision that got you there was not exactly textbook.

Investing works the same way. One lucky market call can feel like evidence that you have a gift. Two lucky calls can make you dangerous. Three can make you start explaining your “process” at dinner parties.

That is where market timing becomes so tempting.

Most Timing Questions Do Not Sound Like Timing Questions

Most people do not walk into a meeting and say, “I would like to abandon my investment plan and make a large tactical asset allocation decision based on my short-term emotional reaction to recent headlines.”

That would be too honest.

Instead, it sounds more reasonable.

“Should we wait until after the election?”

“Should we move to cash since the market is at an all-time high?”

“Should we buy more now because the market is down?”

“Should we reduce stocks until things feel better?”

“Should we wait for the Fed?”

“Should we wait for the recession everyone keeps predicting?”

Those are not bad questions. They are human questions. But many of them are market-timing questions with a more respectable name.

The appeal is obvious. If you could consistently get out before the bad parts and get back in before the good parts, the payoff would be enormous. You would not need a financial plan. You would need a beach house, a satellite phone, and perhaps a tasteful but unnecessary compound in Hawaii.

There is a reason people keep looking for that magic signal. The problem is that the signal tends to look much clearer in hindsight than it does in real time.

The Hard Part Is Getting Back In

One of the hardest parts of investing is accepting that the market and the headlines do not move in a clean, predictable pattern.

A bad headline does not automatically mean stocks will fall. A good headline does not automatically mean stocks will rise. Markets are forward-looking, messy, competitive, and constantly digesting information from investors with different opinions, time horizons, tax situations, and liquidity needs.

Think back to 2020. The world shut down. Businesses closed. People were locked in their houses. The market fell hard and fast. If you had told someone in March 2020 that stocks would soon begin a powerful recovery, you probably would have sounded detached from reality.

But markets do not wait for reality to feel comfortable.

That is the trap. By the time the news feels safe, prices may have already moved. By the time the headlines confirm your fear, the market may be looking past it.

This is also why getting out is only half the decision. You still have to decide when to get back in.

And that second decision is usually harder.

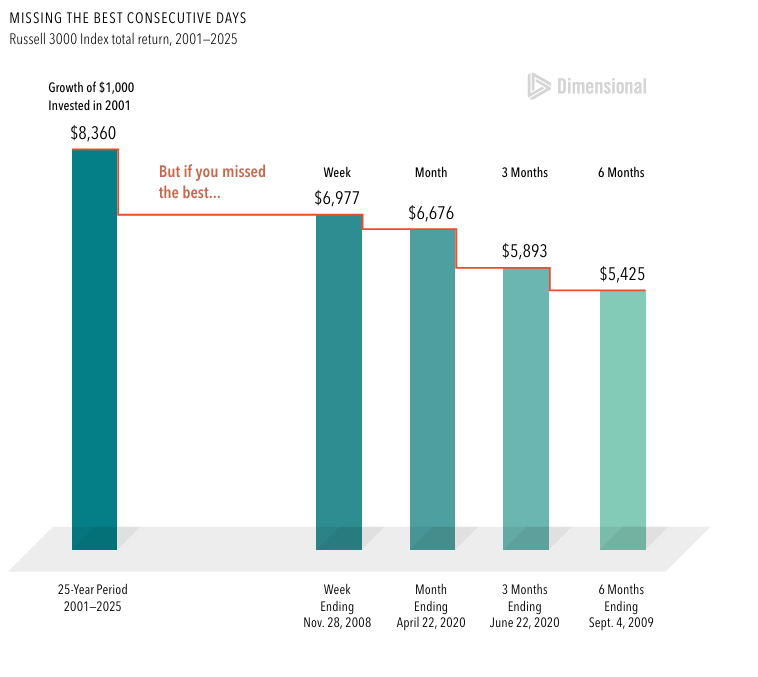

Exhibit 1. The Cost of Missing the Best Consecutive Periods

Source: Dimensional Fund Advisors, “The Cost of Trying to Time the Market.” Russell 3000 Index total return, 2001–2025. Data presented in the Growth of $1,000 exhibit is hypothetical and assumes reinvestment of income and no transaction costs or taxes. The data is for illustrative purposes only and is not indicative of any investment. Indices are not available for direct investment, and their performance does not reflect expenses associated with managing an actual portfolio. Past performance is no guarantee of future results.

Dimensional recently illustrated this point using a hypothetical $1,000 investment in the Russell 3000 Index from 2001 through 2025.

The image shows the math behind a phrase people hear all the time: time in the market tends to matter more than timing the market.

The phrase may be overused, but it is still helpful to remember.

In Dimensional’s example, missing the best three consecutive months reduced the ending value from $8,360 to $5,893. That is not a rounding error. It is a ~54% difference, especially when you remember that the missing growth does not just disappear for that year. You also lose the future compounding on that growth.

That is the part many investors underestimate. Missing a strong rebound does not just hurt once. It can change the base from which every future return compounds.

Of course, this scenario is a hypothetical index example. It is not an actual portfolio, it excludes taxes and transaction costs, and it does not predict future results. Still, the broader lesson is important: being out of the market for even a relatively short period can create a cost that is difficult to recover from.

“The Market Is High” Is Not a Plan

Another common timing argument shows up when markets hit new highs.

I understand the instinct. Buying after a strong run feels like showing up late to a party. Nobody wants to be the last guy walking in with a six-pack right before the cops arrive.

But all-time highs are not rare accidents. They are a normal part of long-term market growth. If stocks are expected to provide a positive return over time, then markets will repeatedly hit new highs along the way. Otherwise, the long-term return would not exist.

That does not preclude the market from falling after hitting a high. Of course it can. It does that all the time. But “the market is high” by itself is not much of a plan.

The better question is whether your allocation fits your goals, time horizon, cash needs, and ability to stay invested when the next decline arrives. If you own stocks only because they have recently gone up, you may not have an investment plan. You may own a mood ring.

Fancy Timing Tools Still Have the Same Problem

There are plenty of timing tools that sound more sophisticated than “I have a bad feeling about this.”

Moving averages are one. Valuation ratios are another. Now we can add machine learning and artificial intelligence to the list. I do not dismiss these tools entirely. Some valuation measures can provide useful context. Some trend measures can be interesting. Some AI tools may help process information more efficiently.

But “interesting” is not the same thing as “actionable.”

Suppose you use a moving average. Which one? Forty days? Two hundred days? When do you sell? When do you buy back? What if the signal changes three times in a few months? What if the strategy works before taxes but fails after taxes?

The more rules you test, the more likely one of them will appear to work by chance. That is not necessarily financial science. Sometimes it is just spaghetti hitting the wall.

And taxes matter. Transaction costs matter. Bid-ask spreads matter. Short-term capital gains matter. In taxable accounts, a timing strategy has to clear a much higher hurdle than the chart on the internet suggests.

This is where smart people can get themselves into trouble. In many parts of life, effort and intelligence are rewarded. Work harder, study more, and improve the result. Investing is strange because trying harder can sometimes make the outcome worse. More activity can mean more taxes, more mistakes, more second-guessing, and more opportunities to abandon a perfectly reasonable plan.

The Better Alternative Is Boring

The alternative to market timing is not doing nothing. It is doing the right things on purpose.

Set an allocation that matches the plan. Diversify broadly. Keep enough in lower-volatility assets for near-term spending needs. Rebalance when appropriate. Harvest losses when available. Be thoughtful about taxes. Adjust the plan when life changes, not every time the market moves.

That may sound boring.

Good.

Boring is underrated.

A portfolio does not need to be exciting to work. In fact, if your portfolio is constantly exciting, something may be wrong. Most families do not need an investment strategy that produces cocktail-party stories. They need a strategy that helps fund retirement, college, charitable giving, housing decisions, taxes, and whatever else life throws at them.

As an Austin financial planner, I spend a lot more time helping people manage behavior, taxes, risk, and tradeoffs than trying to guess next quarter’s market return. That is not because I lack opinions. I have plenty of opinions. Some of them are even useful.

But an opinion is not a plan.

The real planning question is not, “Can we avoid every downturn?” We cannot. The better question is, “Can we build a portfolio and financial plan that gives us a reasonable chance of staying disciplined through the downturns?”

That is a very different exercise.

The Luckiest Trade Is Not a Strategy

There is nothing wrong with having a lucky trade. Enjoy it. Tell the story. Maybe even exaggerate it a little if no one is checking statements.

But do not confuse it with a repeatable process.

The market has a way of humbling people who start believing their own highlight reel. A lucky sale can make cash feel safe right before the rebound. A lucky purchase can make concentration feel smart right before the decline. A lucky forecast can make the next forecast feel inevitable.

That is how a good story becomes a bad plan.

For most investors, the goal is not to win the next market prediction contest. The goal is to make a series of durable decisions that improve your chances over time. That means accepting uncertainty, owning an allocation you can live with, and resisting the urge to treat every headline as an instruction.

If you are not sure whether your portfolio is built around a plan or a collection of market opinions, it may be worth reviewing. If it’s time to review your allocation, tax strategy, or retirement plan, get in touch through the ATX Portfolio Advisors contact page.