The first quarter of 2026 gave investors a timely reminder that markets rarely move in a neat, predictable sequence. US stocks pulled back, developed international stocks held up better, emerging markets were slightly negative but still comparatively resilient, and bonds provided little help. That is not an unusual combination. This is a prime illustration of why discipline often serves long-term investors better than prediction.

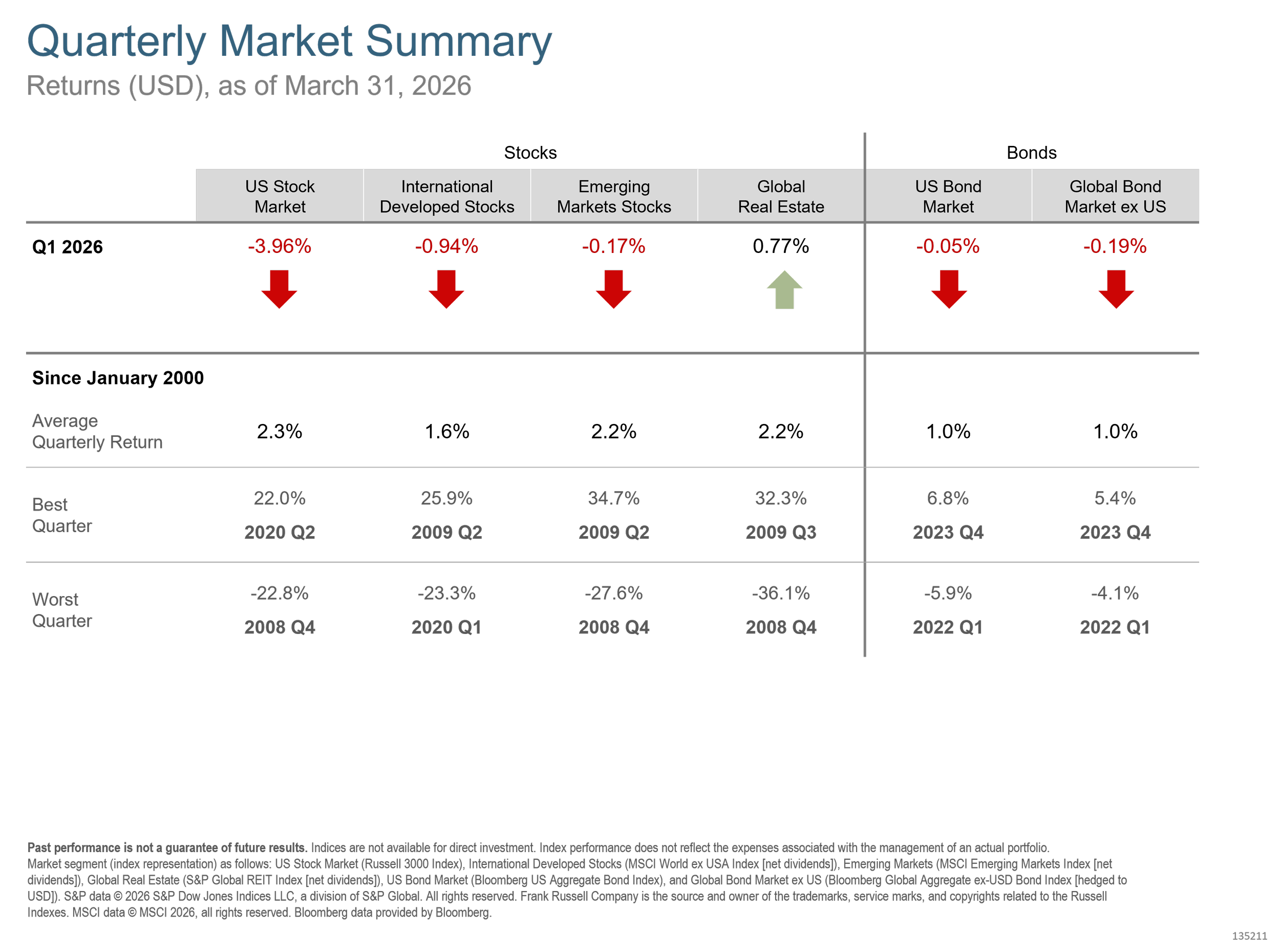

Q1 2026 market summary. US stocks declined 3.96% in the quarter, while international developed stocks fell 0.94%, emerging markets slipped 0.17%, global real estate gained 0.77%, and the US bond market was down 0.05%.

At the headline level, the quarter was difficult for US investors. The US stock market, represented by the Russell 3000 Index, declined 3.96% in the first quarter. International developed stocks fell 0.94%, and emerging markets stocks declined just 0.17%. Global real estate posted a modest gain of 0.77%. On the fixed income side, the US bond market was essentially flat at -0.05%, while global bonds outside the US, hedged to dollars, declined 0.19%.

That mix of returns is worth noticing because it shows how quickly market leadership can rotate. After an extended stretch in which many investors grew accustomed to strong US market leadership, the first quarter offered a different pattern. International markets did not produce strong absolute returns, but they still held up better than the US. That is exactly the kind of quarter that reminds me why global diversification continues to matter.

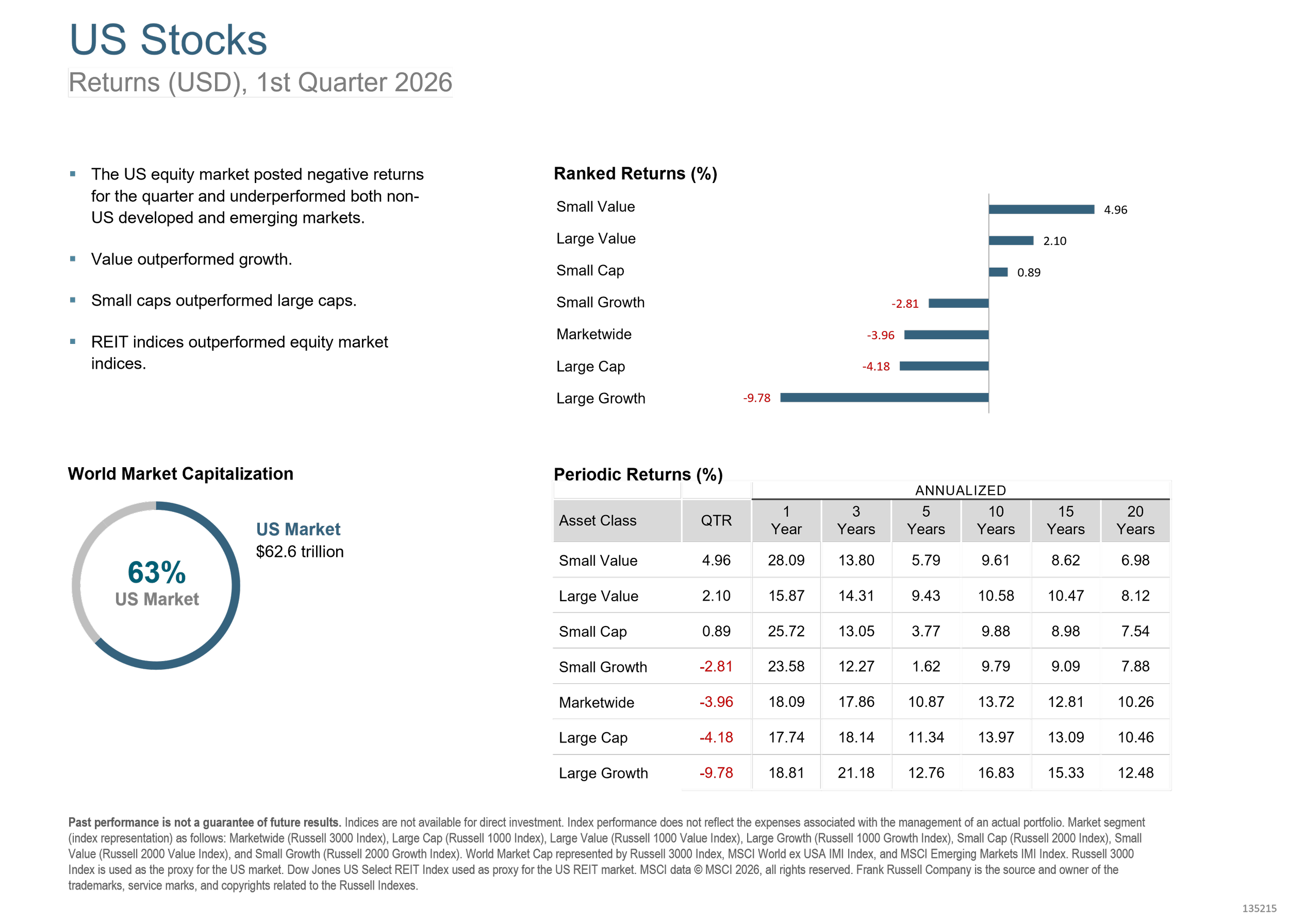

Inside the US market, the story was even more interesting than the broad index return. Value outperformed growth, small caps outperformed large caps, and REITs outperformed the broader equity market. Large growth stocks were the weakest part of the US market, down 9.78% for the quarter, while small value stocks gained 4.96% and large value stocks gained 2.10%. That is a meaningful reversal from the narrow leadership investors had become used to seeing.

US equity returns in Q1 2026 show a sharp spread between value and growth. Small value gained 4.96%, while large growth fell 9.78%, highlighting how different the experience was beneath the headline US market return.

I think that matters for two reasons. First, it is a reminder that broad index returns often hide important differences underneath the surface. Second, it shows why portfolios built only around the biggest and most expensive companies can become more fragile than they appear when market sentiment changes. A diversified allocation does not guarantee a smoother ride every quarter, but it can reduce dependence on one narrow segment of the market.

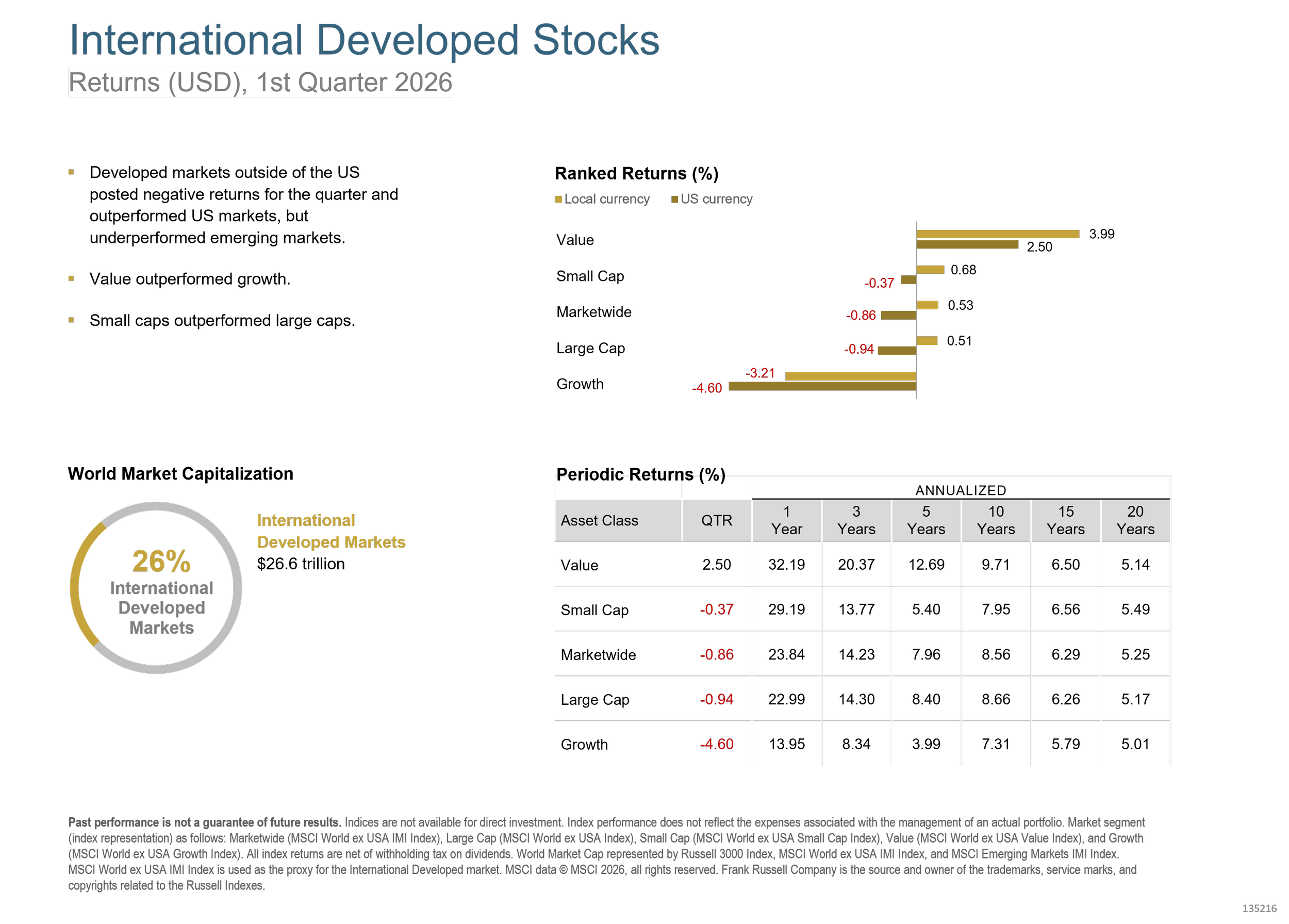

International developed markets told a somewhat similar story, although with less extreme dispersion. Developed markets outside the US posted a quarterly return of -0.86%, which was better than the US. Value outperformed growth there as well. In the deck’s developed-market breakdown, value gained 2.50% for the quarter, while growth declined 4.60%. Small caps were modestly negative at -0.37%, but still held up better than the large-cap benchmark at -0.94%.

International developed markets outperformed the US in Q1 2026, with value stocks leading and growth stocks lagging.

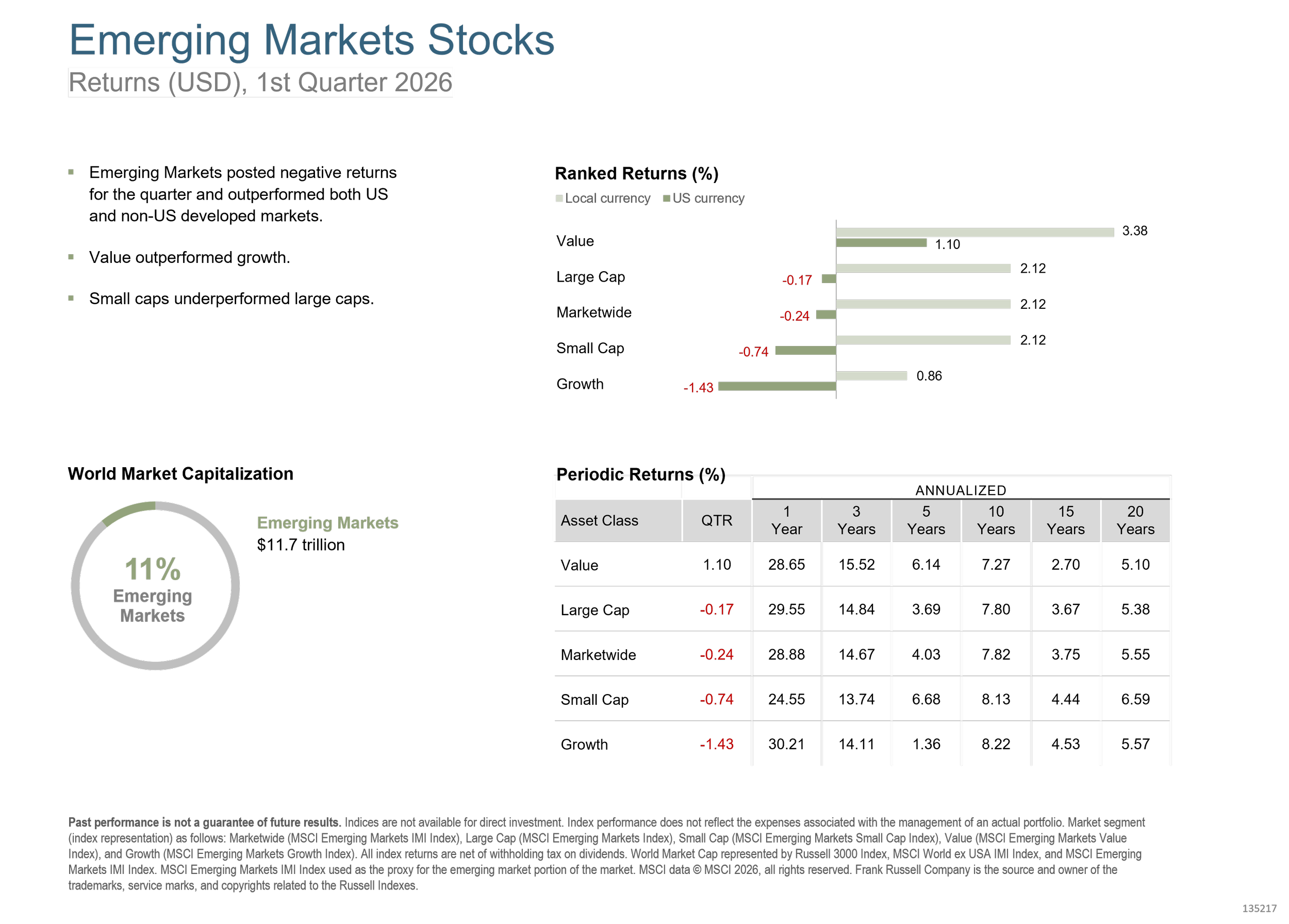

Emerging markets were also a positive reminder that leadership does not always come from the places investors expect. The broad emerging markets category declined just 0.24% in the quarter, outperforming both the US and developed international markets. Within emerging markets, value held up best at 1.10%, while growth declined 1.43%. Small caps lagged large caps, but the overall result was still comparatively resilient.

Emerging markets were slightly negative in Q1 2026, but they still outperformed both the US and developed international markets. Value held up better than growth.

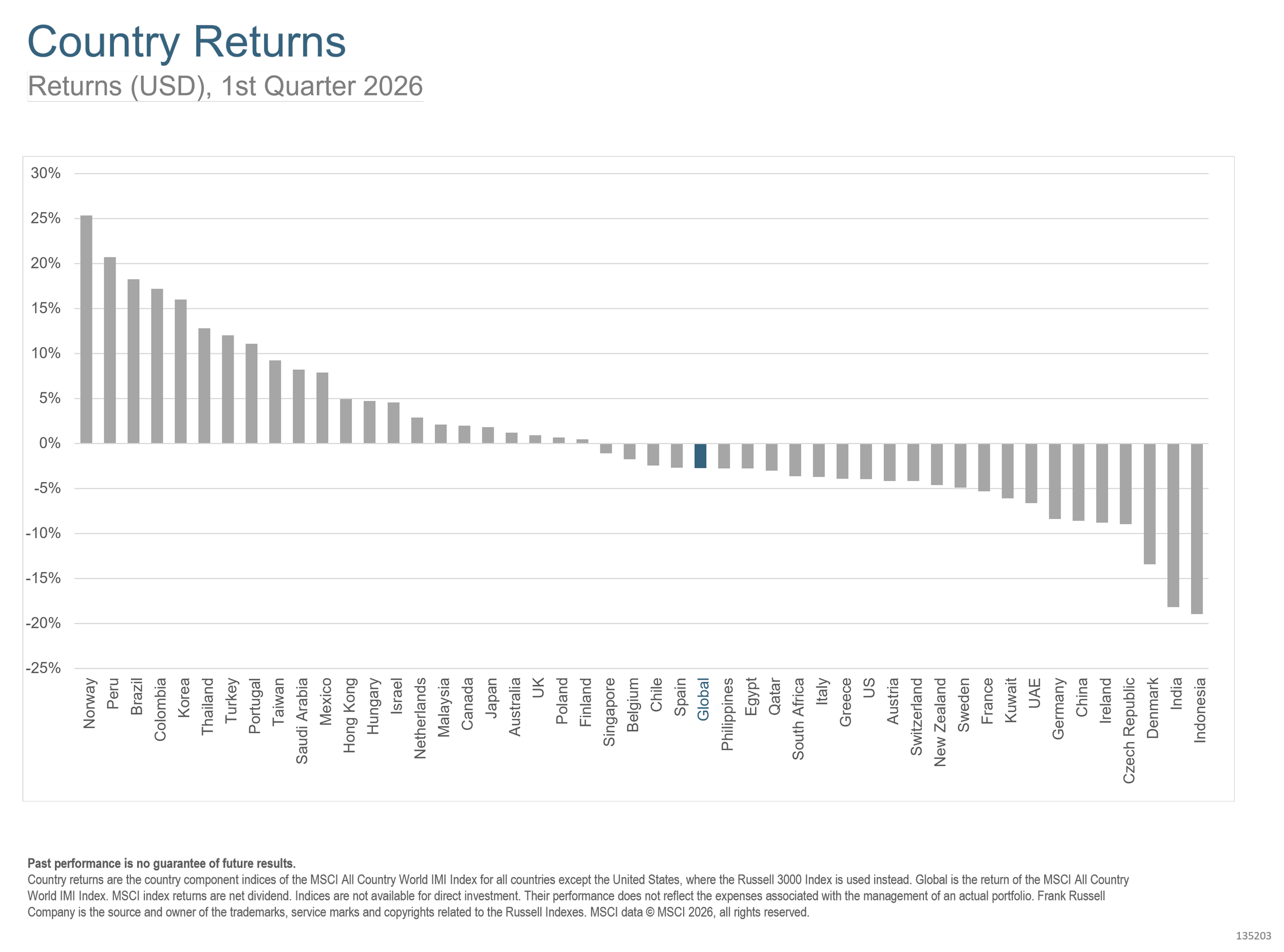

At the country level, dispersion was wide. The strongest quarter-end results came from markets such as Norway, Peru, Brazil, Colombia, Korea, and Thailand, while weaker results included Denmark, India, and Indonesia. The US landed in the lower half of the distribution at -3.96%. These kinds of country-level spreads are another reason I am generally skeptical of concentrated geographic bets. It is very difficult to predict which markets will lead over short windows, and leadership often comes from places investors were not focused on at the start of the quarter.

Country returns were widely dispersed in Q1 2026, reinforcing the case for broad global diversification rather than concentrated country bets.

Bonds were not especially helpful, but they also were not the main story. The Bloomberg US Aggregate Bond Index was down 0.05% in the quarter. Interest rates generally increased during the quarter, with the 10-year US Treasury yield rising to 4.30% and the 30-year Treasury yield ending at 4.88%. Shorter-term fixed income held up better than longer maturities, which is consistent with what investors would expect in a rising-rate environment.

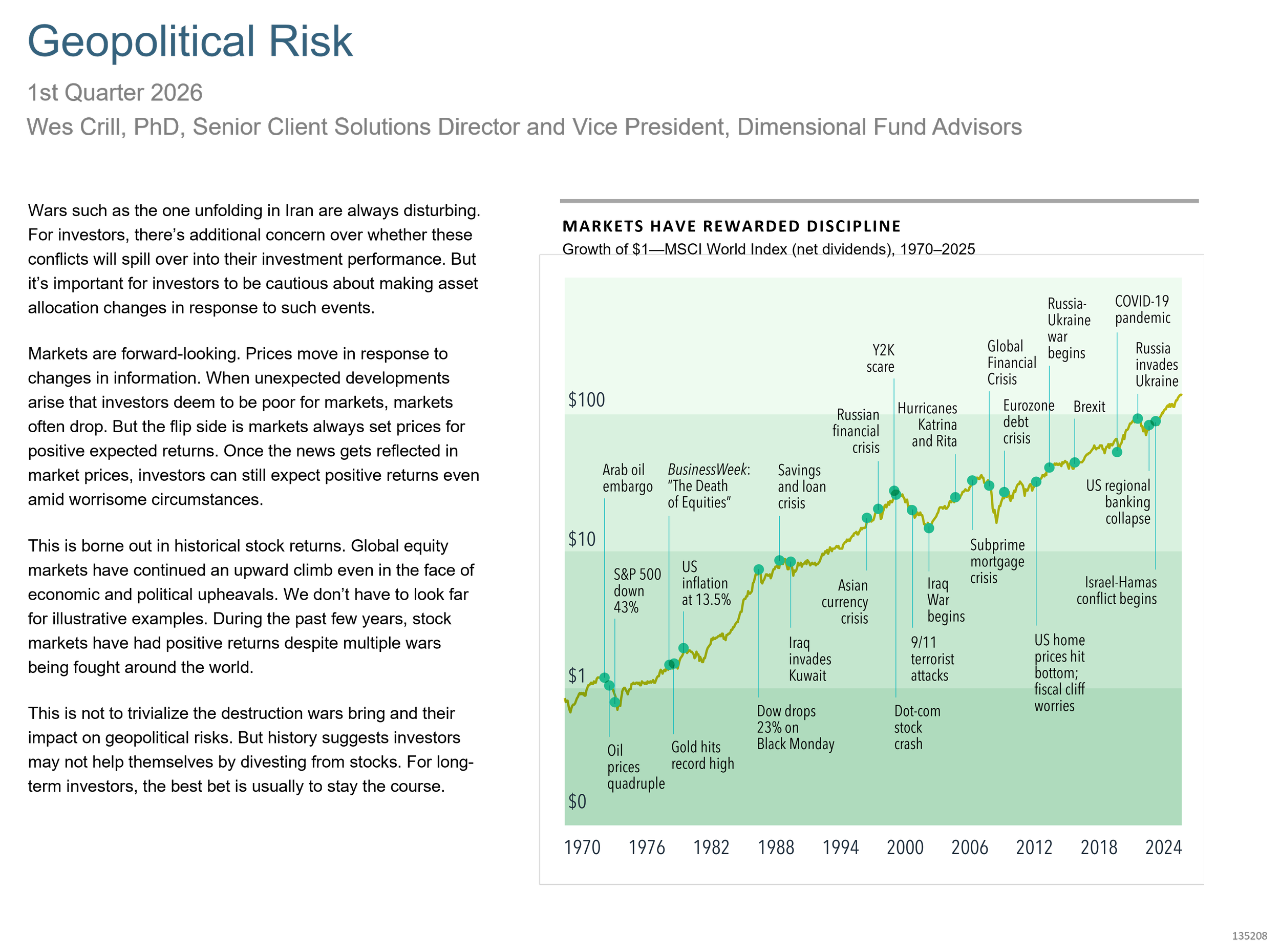

Middle East war and the related geopolitical shocks are disturbing and real, but investors should be cautious about changing their asset allocation in response. Markets are forward-looking. When bad news arrives, prices adjust quickly. But once that repricing occurs, expected returns do not disappear simply because the headlines remain unsettling.

Past performance is no guarantee of future results.

Geopolitical risk can be unsettling, but history suggests that investors typically benefit more from maintaining discipline than from altering allocations based on current events.

That is the practical lesson from this quarter. A pullback in US stocks, better relative performance abroad, and a reversal in style leadership are not signals that a long-term plan is broken. They are reminders that a diversified portfolio is designed precisely for periods when leadership shifts unexpectedly. Some quarters reward patience quickly. Others test it first.

For long-term investors, especially those approaching or living in retirement, the better response is usually not to chase what just worked or abandon what just disappointed. It is to revisit the plan, check whether the current allocation still fits the job it was built to do, and rebalance thoughtfully when appropriate. Good investment management is usually less about forecasting the next quarter and more about maintaining a structure that can survive many different kinds of quarters.

The first quarter of 2026 was uncomfortable for US investors, but it was also constructive in one important sense: it reminded us that diversification still works, valuation still matters, and discipline still has real value. If your portfolio has drifted, or if your investment plan has not been reviewed in a while, the present moment is a reasonable time to take a fresh look. A thorough review should connect the allocation back to your retirement plan, spending needs, and long-term goals rather than to whatever headline happens to dominate the moment.