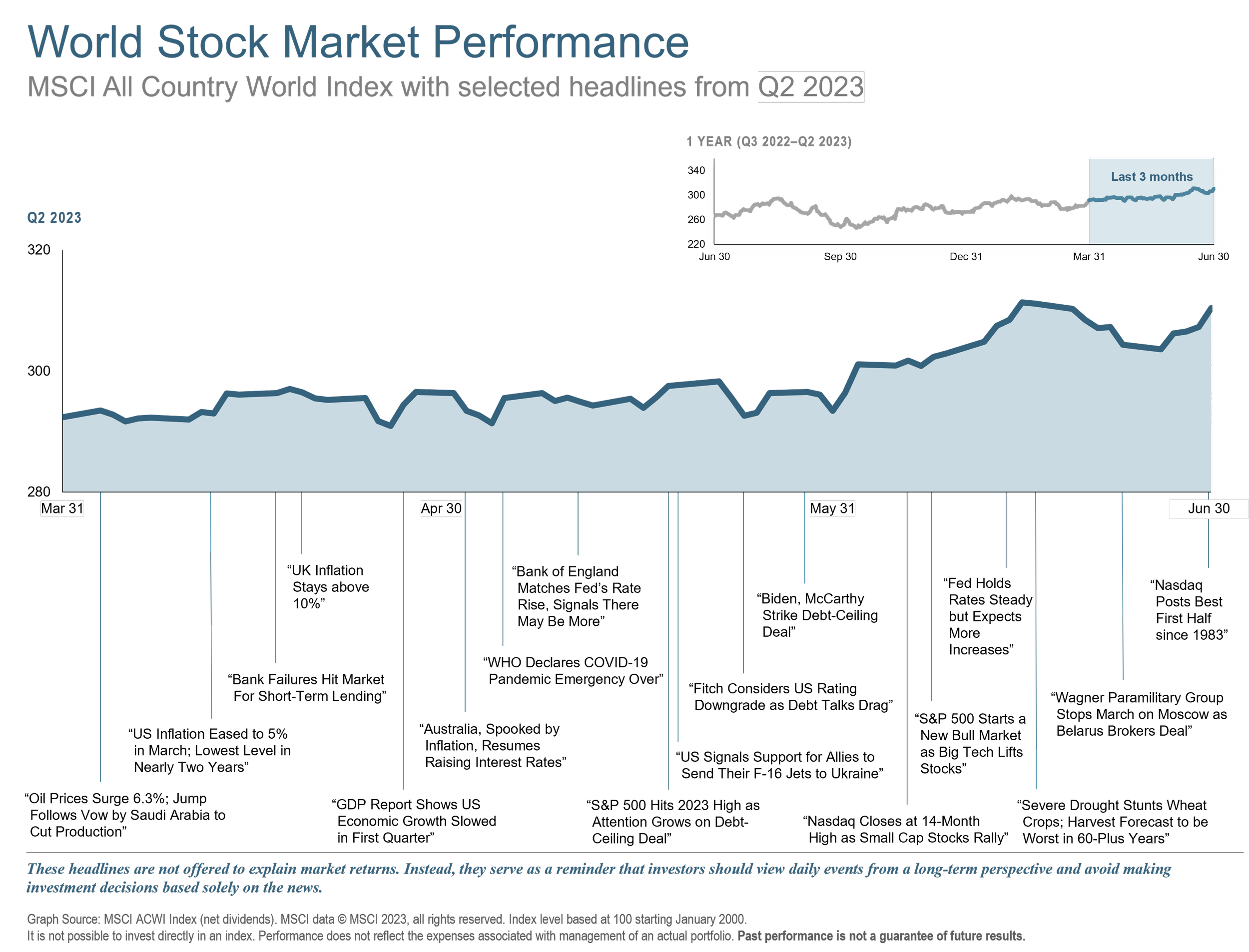

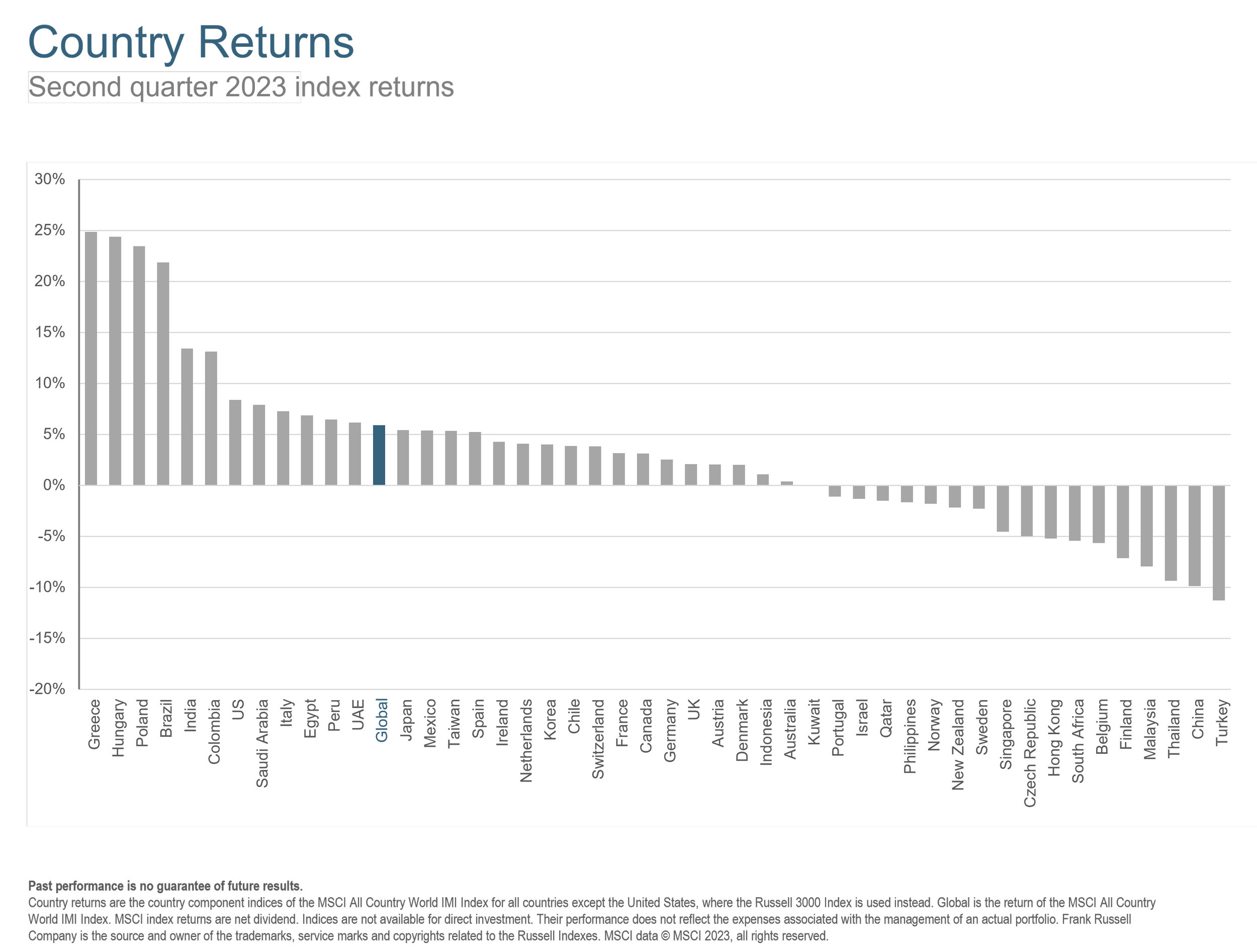

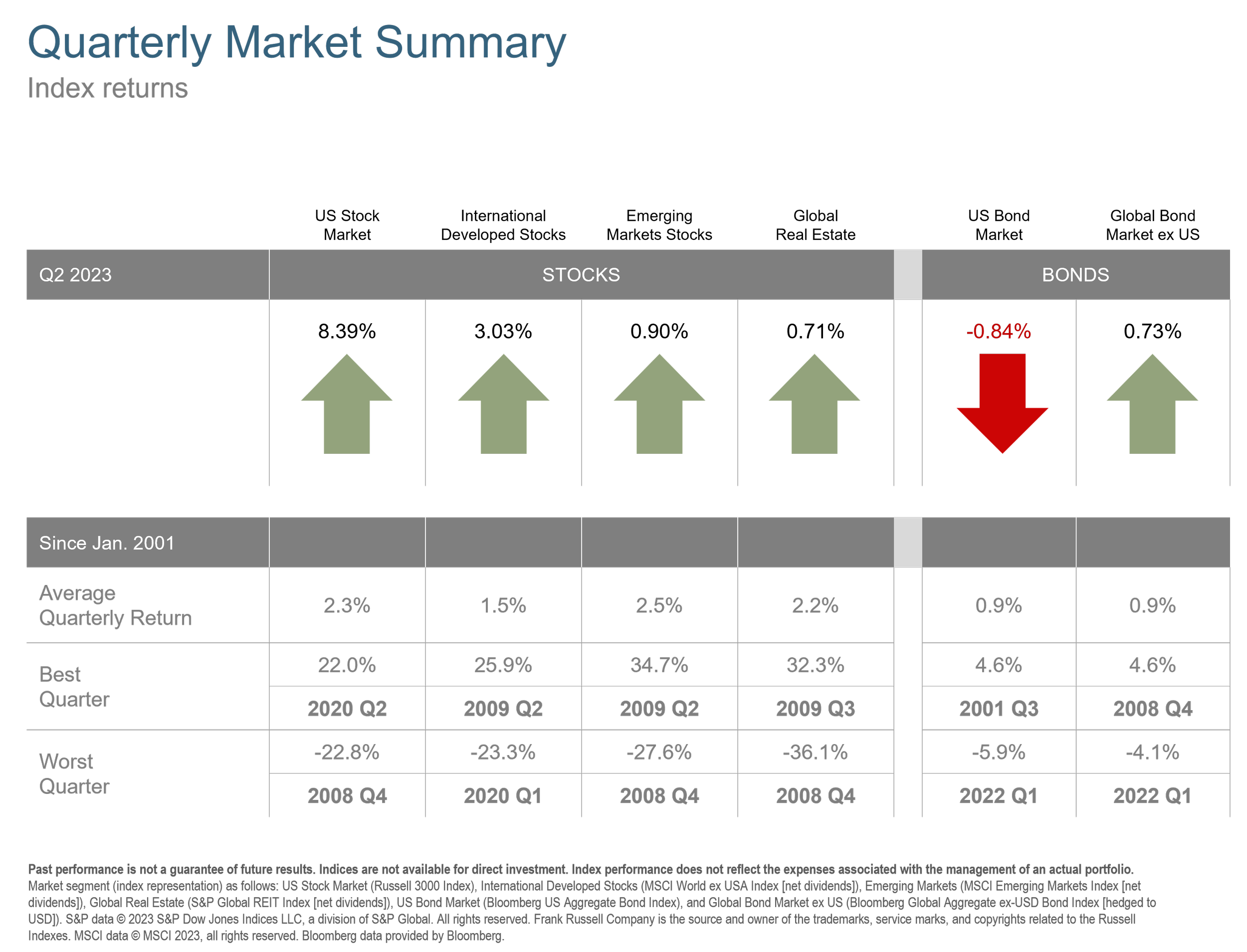

Global stocks continued their recovery from last year's downturn, with the MSCI All Country World IMI Index (up around 6% in Q2) outperforming global bonds (Bloomberg Global Aggregate Bond Index) for the third consecutive quarter. Inflation worries in the US continued to temper with the 5-year expectation currently around 2.5% as measured by breakeven rates in the TIPS market. Volatility also trended down with the VIX (CBOE Volatility Index) falling to year-to-date lows in June.

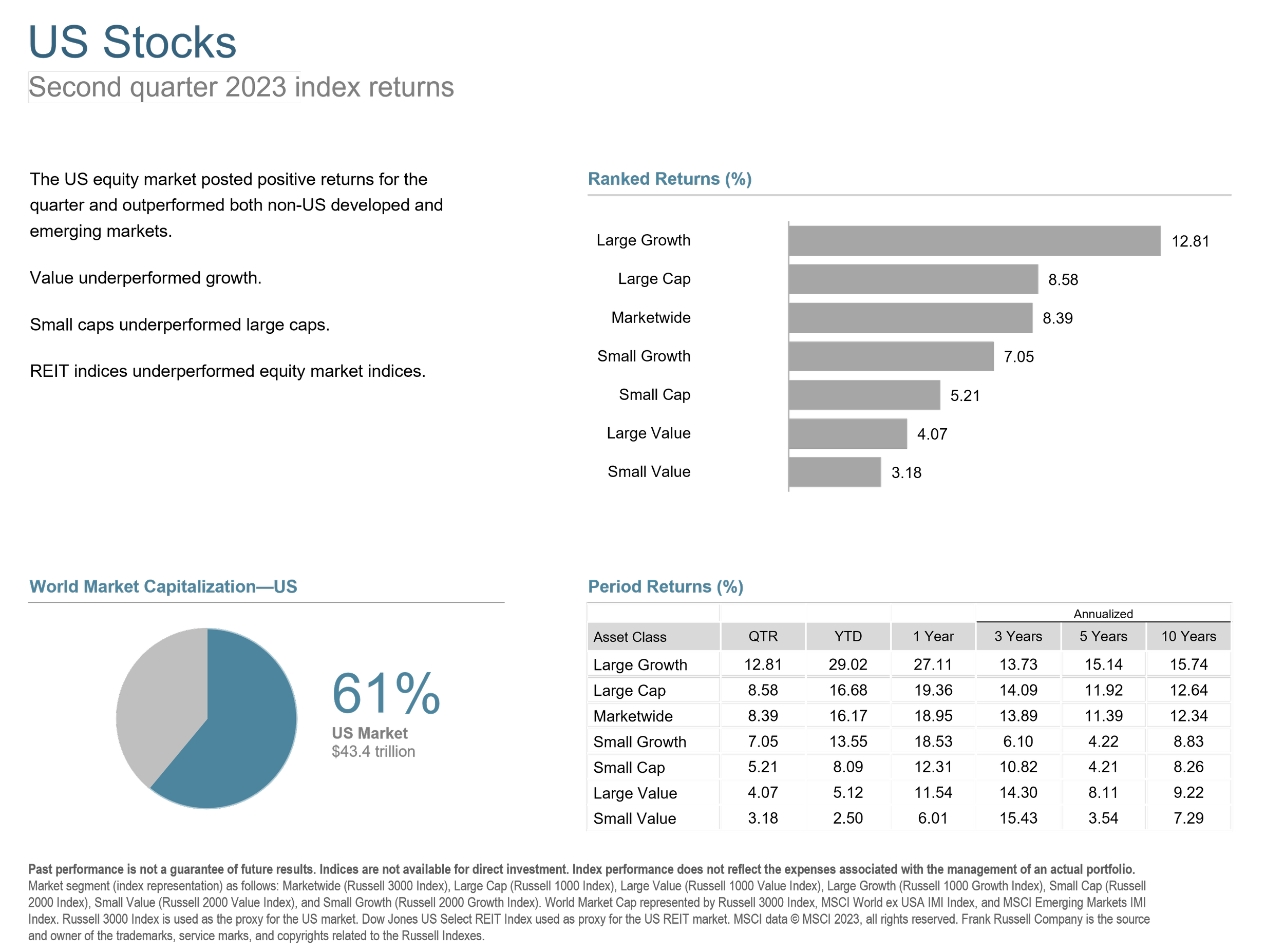

Technology names like NVIDIA (up over 50%), Tesla (up > 25%), and Netflix (up > 25%) led the quarter, lifting the returns of large growth stocks, while value-oriented sectors like energy and financials lagged.

Every factor we emphasize in ATX Portfolio Advisors model portfolios underperformed in the quarter with large companies beating small by over 3%, growth beating value by over 3%, and low profitability stocks beating high profitability around 1.5%.

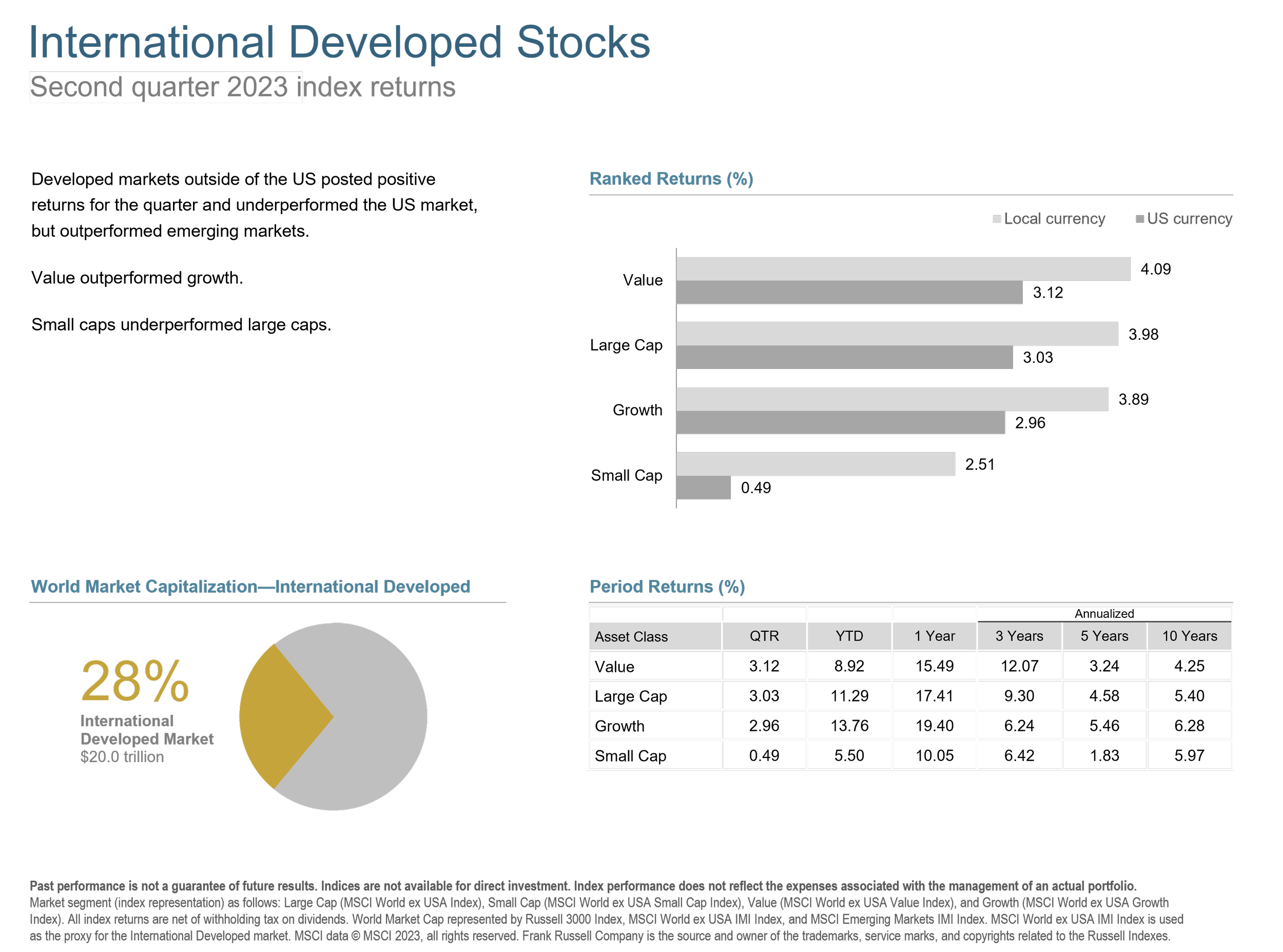

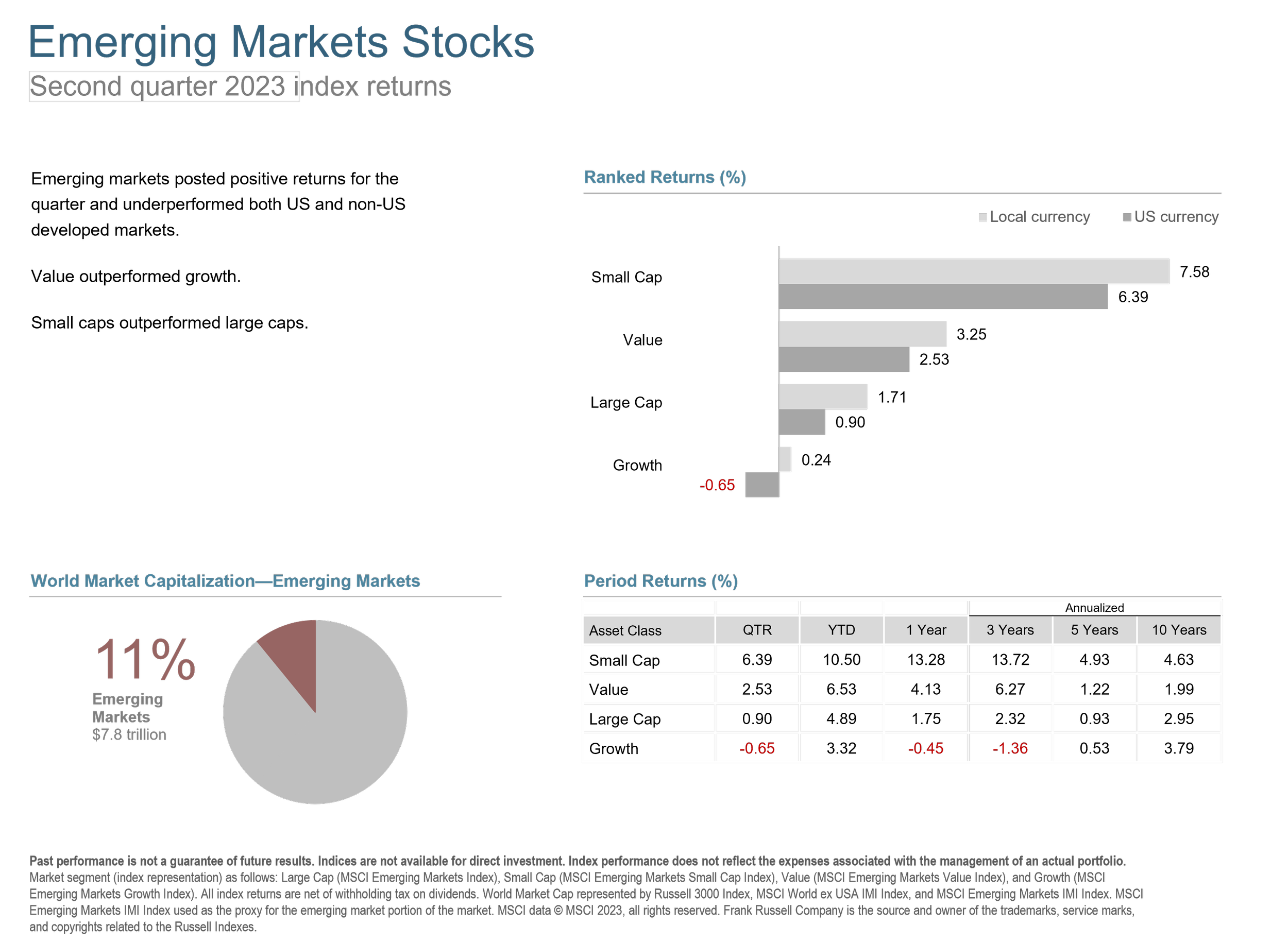

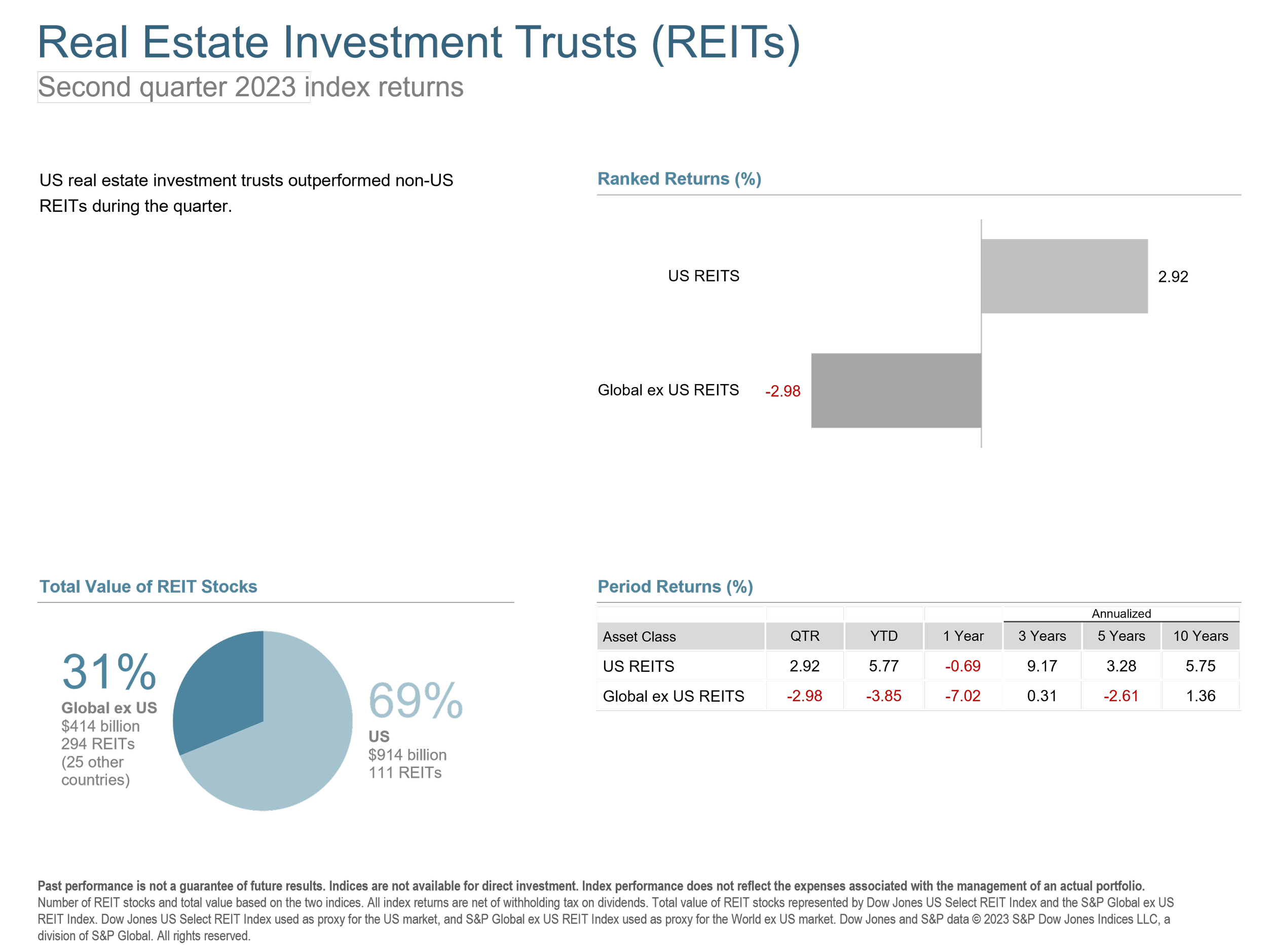

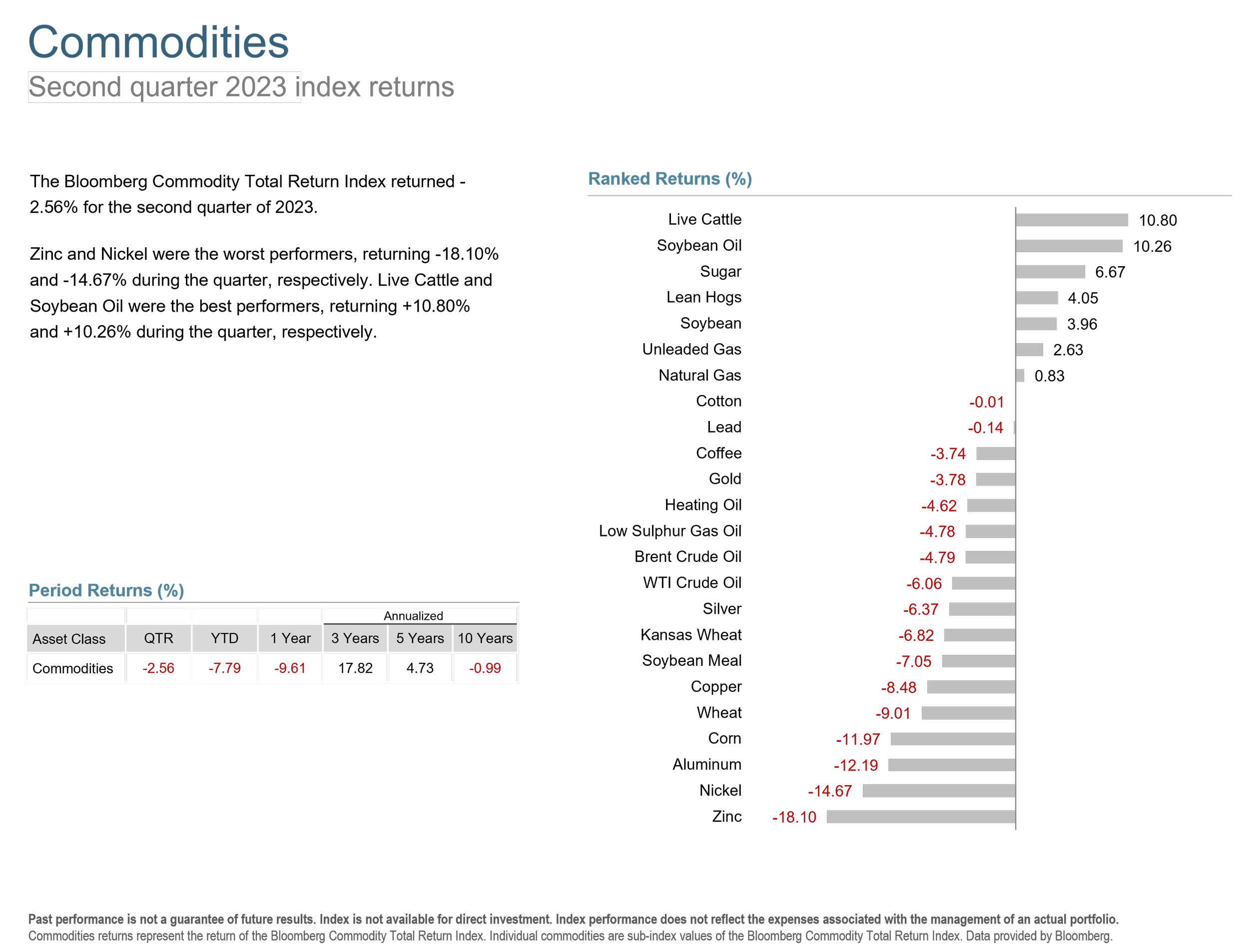

Real Estate and Materials were the worst performers, ending the quarter down by around .4% and .5%, respectfully. International developed markets saw positive value performance yet faced negative size and profitability premiums. Emerging market stocks lagged developed markets but the premium environment was slightly more favorable, as small and value stocks outperformed while more profitable stocks—while negative overall—outperformed within small caps.

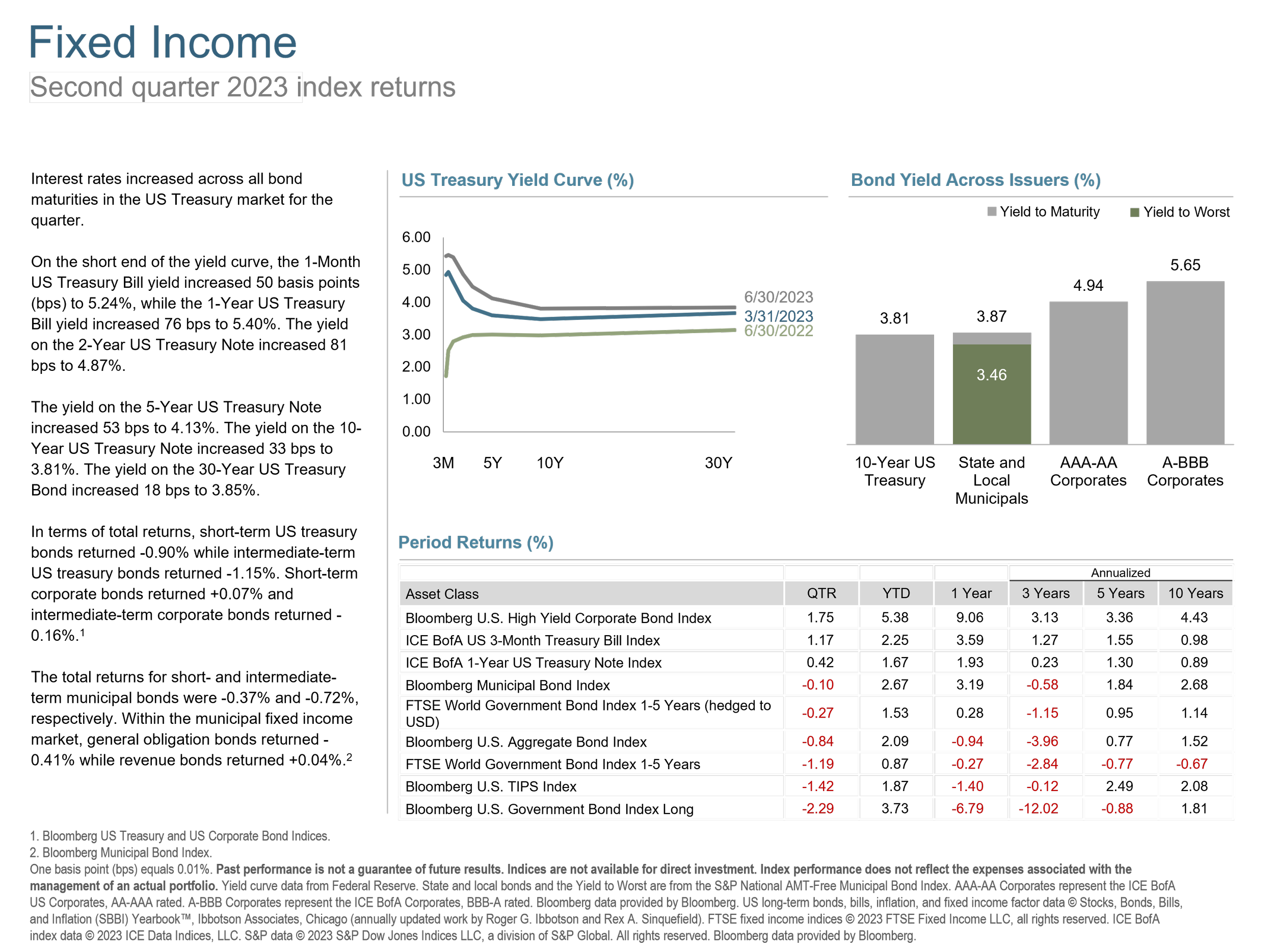

In May, the US Consumer Price Index (CPI) fell to 4.9% year-over-year, its lowest annual rate in more than two years. Low unemployment, which perversely has been bad for the market when good numbers are reported, remained strong in June at 3.5%. The Federal Reserve held its key fed funds rate steady at 5-5.25% in June after 10 consecutive rate hikes since March of 2022. The Fed also continued their quantitative tightening program with their balance sheet now shrinking by about $95 billion per month to a current level of “just” $7.7 trillion as of yesterday.

Some of the fears raised earlier this year by the runs on regional banks seem to have abated. However, we continue to recommend tactical steps such as keeping balances at banks below FDIC limits and investing cash directly in other instruments like US Savings Bonds, Treasury Bills, and money markets not only to improve credit exposure but also to increase yields. As always, we should use our investment plans to inform the real impact of the risks we are taking as it helps to tune out the noise that current headlines always create, allowing us to focus on time-tested principles to avoid making shortsighted missteps.

If you would like to review your plan, get in touch. In the meanwhile, you can see the slides below for a visual review of Q2 2023.