The US Constitution vests the US Congress with the power of the purse through Article I, Section 9, Clause 7 (the Appropriations Clause) and Article I, Section 8, Clause 1 (the Taxing and Spending Clause). This power was explicitly bestowed by the founders of our country as a check and balance for an executive who may be inclined to spend resources irresponsibly.

Congress exercises this power by passing an annual budget and also by authorizing borrowing by the US Treasury (part of the Executive Branch) if the spending exceeds tax revenue. It is this borrowing authorization that is known as "the debt ceiling", but most of us would liken it to the credit limit extended by our bank. Congress has increased this credit limit 78 times since 1960, although in recent years, this process has occasionally become a cudgel for both parties to leverage political concessions when one controls Congress but the other occupies the White House.

Historically, ignoring this drama would have served you well as an investor. However, it is fair to question what the impact may be if the two sides cannot come to a political consensus. The US effectively reached its credit limit in January, which triggered "extraordinary measures" (also known as accounting) by the Treasury Department to continue servicing debts and obligations. According to Treasury Secretary Yellen, the government will have exhausted all of its accounting measures by June 1 and will run out of cash to pay its bills soon thereafter.

Perhaps the most immediately impacted would be federal workers, who are counting on their paychecks. Next up are holders of US Treasury bonds that have interest and/or principal payments due. It will also likely become a talking point by the President that Social Security, Medicare, and military expenditures are at risk, although some payments are considered "mandatory" versus others that are discretionary, so this is likely more theater than substance.

We are already seeing the impact on markets. Shorter-term US Treasury bills and bonds have dropped in price (and the yields are up over 5%) as the normal certainty of the "full faith and credit" of our country is called into doubt. Holders of these bonds could see delays in payments if the two sides can’t reach consensus before principal and interest are due.

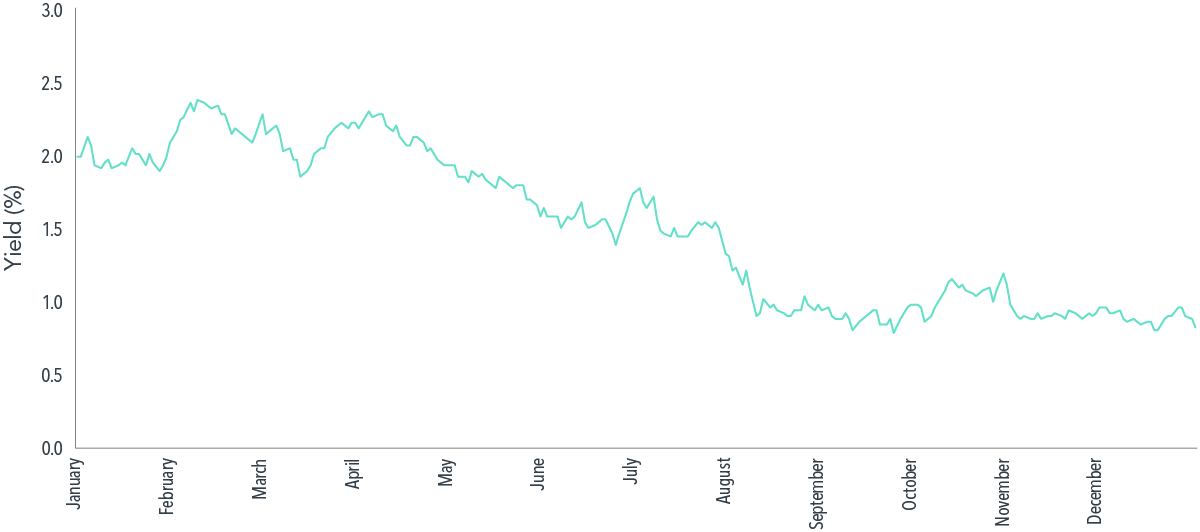

It is likely that as we near June 1 with no deal, the volatility in both the stock and bond markets may increase. Although it is difficult to predict in what direction volatility may trend, Back in the August 2011 debt ceiling crisis, US Treasury prices increased (yields dropped) despite a credit rating downgrade from S&P (Exhibit 1). Global stocks, on the other hand, fell sharply.

Exhibit 1. Falling Yield

Daily 5-Year US Treasury Yield, 2011

Past performance is no guarantee of future results. *Based on ICE BofA MOVE Index, a yield-curve-weighted index of normalized implied volatility on 1-month Treasury options

Data sourced from Bloomberg on May 18, 2023. ICE BofA index data © 2023 ICE Data Indices, LLC.

Of course, we can’t predict the future based on past performance, but we can use that experience to inform our choices. The lesson I have learned over three decades of closely observing markets is that market volatility is the price we pay for taking risks. Trying to outguess the market’s collective wisdom is a fool’s errand.

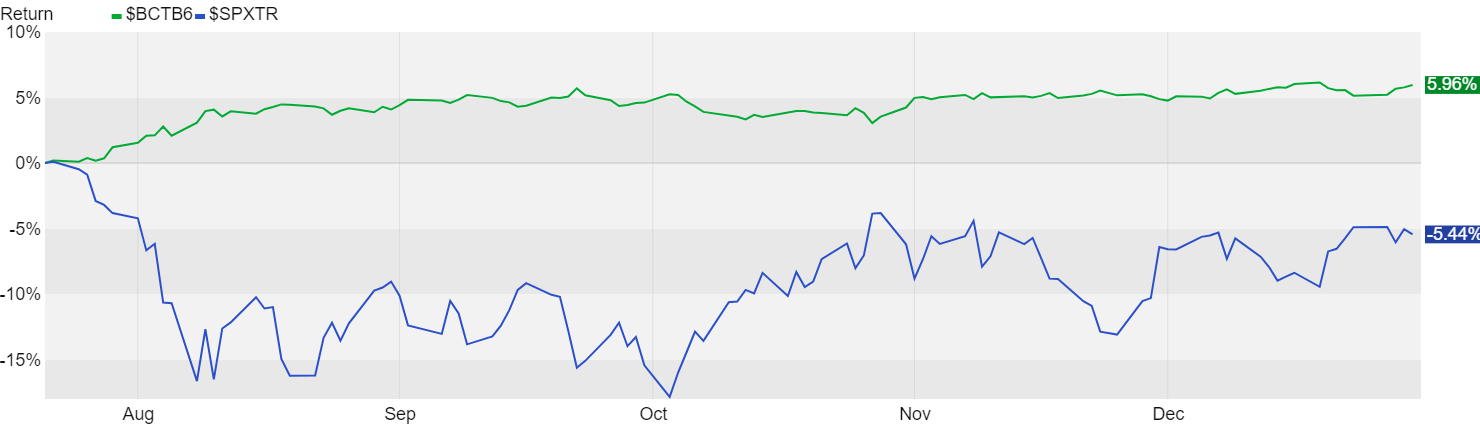

Take that same August 2011 "crisis" period as an example. Had you been lucky enough to move your money out of the stock market into US Treasury Bonds just before the S&P 500 fell on July 22, 2011, you would have felt pretty smug at year's end, outpacing stocks by about 10%. (Exhibit 2.)

Exhibit 2. Perfect Timing

S&P 500 vs US Treasuries 7/22/2011 - 12/31/2011

Past performance is no guarantee of future results. *Based on the S&P 500 vs Barclays US Treasury 5-7 Year Index

Data sourced from Kwanti Analytics on May 25, 2023.

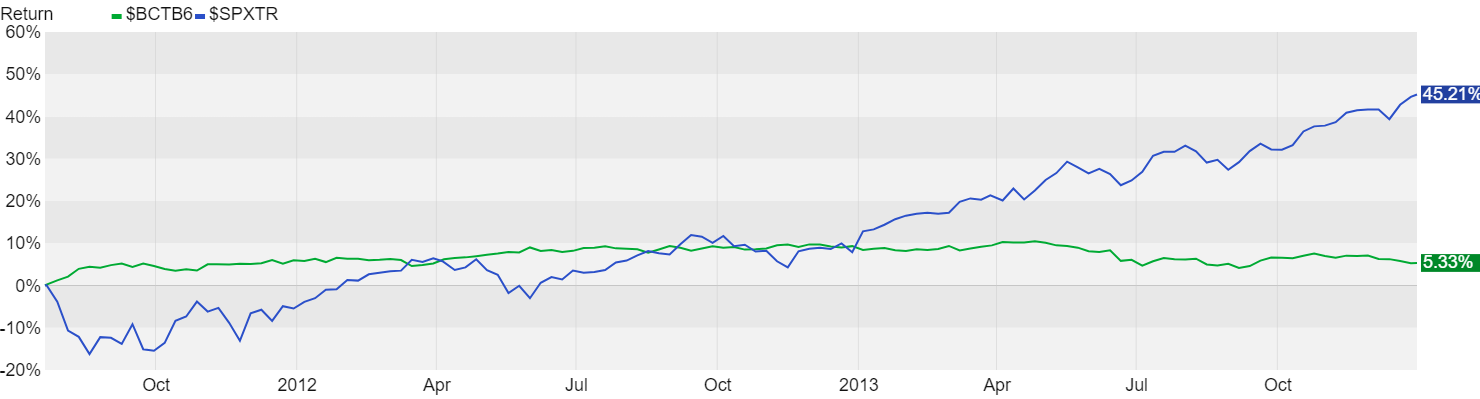

Even though there was another “Debt Ceiling Crisis” in 2013, had you stayed the course all along, your stock portfolio would have outpaced US Treasury bonds by nearly 40% by the end of 2013. (Exhibit 3.)

Exhibit 3. Perfect Timing vs Staying the Course

S&P 500 vs US Treasuries 7/22/2011 - 12/31/2013

Past performance is no guarantee of future results. *Based on the S&P 500 vs Barclays US Treasury 5-7 Year Index

Data sourced from Kwanti Analytics on May 25, 2023.

If history has taught us anything, it is that the stock market can act very unpredictably in the short term. Thus, if you plan to use funds in the next couple of years, you probably should reduce that uncertainty by investing in very short-term types of accounts such as a bank or money market account (yields around 5% are available right now).

But if your plan is for a longer period, this current "crisis" will likely pass soon. A diversified investment portfolio with a disciplined plan that informs decisions is the best tool I know for staying the course.

If you need to create or review your plan, get in touch.