In this week's Accountable Update, the plan was to write about what I was going to do with my $1.5 billion in lottery winnings. However, after reading the fine print that said the actual lump sum jackpot was only around $930 million, I decided to pass on playing.

If you are a politician that passes laws that allow a game to report that 93 cents is actually worth $1.50 to entice more players, you get re-elected. If you are an investment advisor that tries that, like Bernie Madoff for example, you get 150 years in prison! At least most of Madoff's victims got about 75% of their money back. Do you think that's the case with the majority of lotto players?

So, instead, we'll look back at 2015. I start by sharing an article from Weston Wellington of Dimensional Fund Advisors in his Down to the Wire series. In "A Vanishing Value Premium?", he delves into the recent under-performance of value stocks.

The second section is similar to my quarterly market updates, but it reviews both economic and market events from the whole year. It is cleverly titled, "2015 Review: Economy & Markets".

As always, if recent market events have you questioning how you are invested or if your current advisor is the only one making money when your accounts are down, get in touch for a free portfolio review or to discuss ACCOUNTABLE WEALTH MANAGEMENT℠.

A Vanishing Value Premium?

Weston Wellington, Down to the Wire

Vice President, Dimensional Fund Advisors

Value stocks under-performed growth stocks by a material margin in the US last year. However, the magnitude and duration of the recent negative value premium are not unprecedented. This column reviews a previous period when challenging performance caused many to question the benefits of value investing. The subsequent results serve as a reminder about the importance of discipline.

Measured by the difference between the Russell 1000 Growth and Russell 1000 Value indices, value stocks delivered the weakest relative performance in seven years. Moreover, as of year-end 2015, value stocks returned less than growth stocks over the past one, three, five, 10, and 13 years.

Unsurprisingly, some investors with a value tilt to their portfolios are finding their patience sorely tested. We suspect at least a few will find these results sufficiently discouraging and may contemplate abandoning value stocks entirely.

Total Return for 12 Months Ending December 31, 2015

Russell 1000 Growth Index 5.67%

Russell 1000 Value Index−3.83%

Value minus Growth−9.49%

Before taking such a big step, let’s review a previous period when value strategies under-performed to gain some perspective.

As many growth stocks and technology-related firms soared in value in the mid- to late 1990s, value strategies delivered positive returns but fell far behind in the relative performance race. At year-end 1998, value stocks had under-performed growth stocks over the previous one, three, five, 10, 15, and 20 years. The inception of the Russell indices was January 1979, so all the available data (20 years) from the most widely followed benchmarks indicated superior performance for growth stocks. To some investors, it seemed foolish for money managers to hold “old economy” stocks like Caterpillar (−3.1% total return for 1998) while “new economy” stocks like Yahoo! Inc. appeared to be the wave of the future (743% total return for 1998).

Many value-oriented managers counseled patience, but for them the worst was yet to come. In 1999, growth stocks shone even brighter as value trailed by the largest calendar year margin in the history of the Russell indices—over 25%.

Total Return for 1999

Russell 1000 Growth Index 33.16%

Russell 1000 Value Index 7.36%

Value minus Growth−25.80%

In the first quarter of 2000, growth stocks bolted out of the gate and streaked to a 7% return while value stocks returned only 0.48%. As of March 31, 2000, value stocks had under-performed growth stocks by 5.61% per year for the previous 10 years and by 1.49% per year since the inception of the Russell indices in 1979. A Wall Street Journal article appearing in January profiled a prominent value-oriented fund manager who regularly received angry letters and email messages; his fund shareholders ridiculed him for avoiding technology-related investments. Two months later he was replaced as portfolio manager amidst persistent shareholder redemptions.

With value stocks falling so far behind in the relative performance race, it seemed plausible that value stocks would need a lifetime to catch up, if they ever could.

It took less than a year.

By November 2000, value stocks had delivered modestly higher returns than growth stocks since index inception (21 years, 11 months). By month-end February 2001, value stocks had outperformed growth over the previous one, three, five, 10, and 20 years and since-inception periods.

The reversal was dramatic. Over the period April 2000 to November, value stocks outperformed growth stocks by 26.7% and by 39.7% from April 2000 to February 2001.

This type of result is not confined to the technology boom-and-bust experience of the late 1990s. Although less pronounced, a similar reversal took place following a lengthy period of value stock under-performance ending in December 1991.

We can find similar evidence with other premiums:

• From January 1995 to December 1999, the annualized size premium was negative by approximately 963 basis points (bps), amounting to a cumulative total return difference of approximately 113%. Within the next 18 months, the entire cumulative difference had been made up.

• From January 1995 to December 2001, the annualized size premium was positive by approximately 157 bps.

The moral of the story?

Prices are difficult to predict at either the individual security level or the asset class level, and dramatic changes in relative performance can take place in a short period of time.

While there is a sound economic rationale and empirical evidence to support our expectation that value stocks will outperform growth stocks and small caps will outperform large caps over longer periods, we know that value and small caps can under-perform over any given period. Results from previous periods reinforce the importance of discipline in pursuing these premiums.

References

Pui-Wing Tam, “A Fund Manager Sticks to His Values, Loses Customers,” Wall Street Journal, January 3, 2000.

Paul J. Lim, “Oakmark Ousts Manager Sanborn,” New York Times, March 22, 2000.

Standard & Poor’s Stock Guide, January 1999.

Past performance is not a guarantee of future results. Indices are not available for direct investment; therefore, their performance does not reflect the expenses associated with the management of an actual portfolio. A basis point (BP) is one hundredth of a percentage point (0.01%).

There is no guarantee investing strategies will be successful. Investment risks include loss of principal and fluctuating value. Small cap securities are subject to greater volatility than those in other asset categories.

2015 Review: Economy & Markets

The US economy and broad market showed modest gains during the year, although investor discipline was tested by news of a global economic slowdown, rising market volatility in China and emerging markets, falling oil and commodities prices, and higher US interest rates.

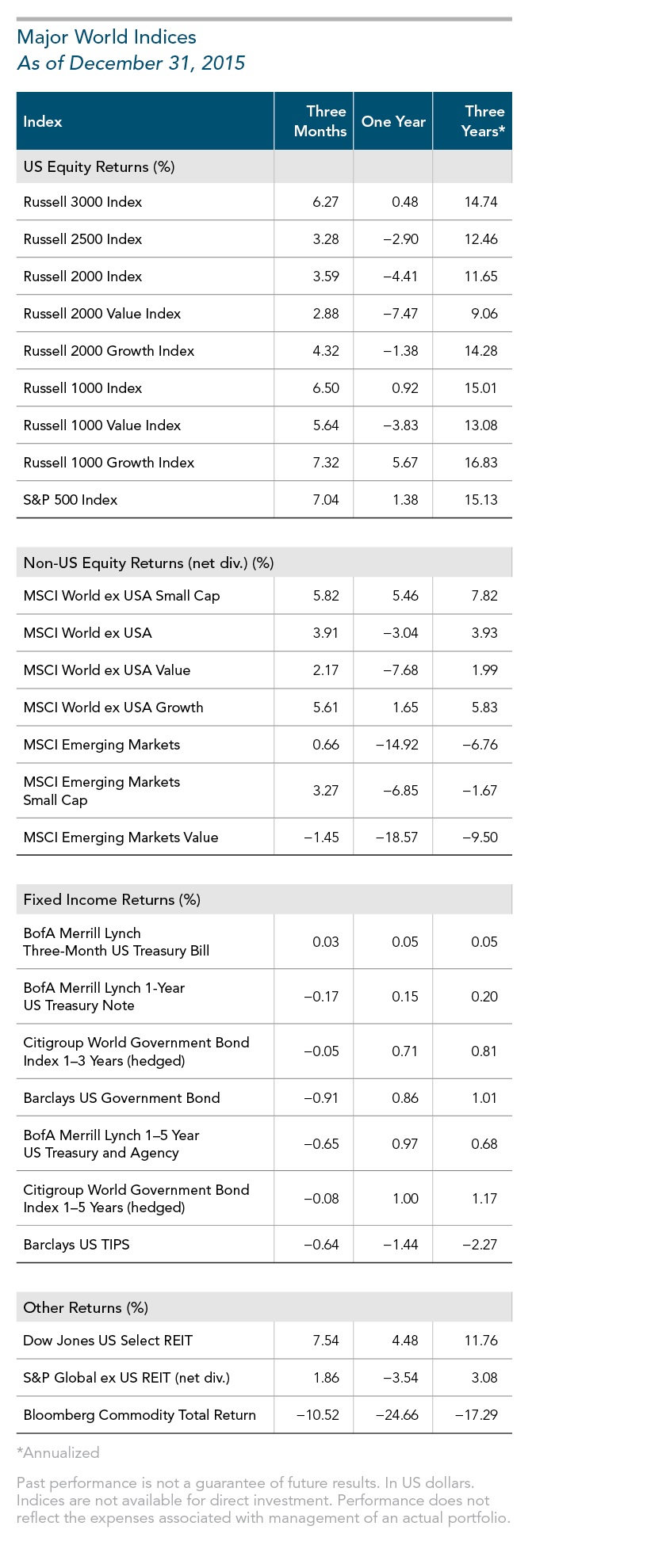

The S&P 500 Index logged a 1.38% total return. The returns across US indices were mixed, but overall the broad US market, as measured by the Russell 3000, gained 0.48%—its lowest return since the 2008 market downturn. The Nasdaq Composite Index returned 6.96%. Performance among non-US markets was mostly negative: The MSCI World ex USA Index logged a ‒3.04% total return and the MSCI Emerging Markets Index a ‒14.92% return (net dividends, in USD). The US dollar’s strong performance against major currencies resulted in lower returns for US investors in various markets. For example, the MSCI All Country World Index returned 1.27% in local currency but ‒2.36% in USD (net dividends).

For most of the year, investors considered the potential impact of higher US interest rates triggered by a US Federal Reserve Bank (Fed) rate increase. The Fed’s announcement finally came in December and by year-end, the yield on the benchmark 10-year Treasury note stood at 2.27%, up from 2.17% in 2014. The Barclays US Government Bond Index returned 0.86% and Barclays US Intermediate Corporate Index returned 1.08%. Global government bonds had slightly positive returns with the Citigroup World Government Bond 1–5 Year Index (USD hedged) returning 1.00%. Global corporate bonds also had positive returns, with the Barclays Global Aggregate Corporate Bond Index 1–5 Years (hedged to USD) returning 1.21%.

The chart above highlights some of the year’s prominent headlines in context of broad US market performance, measured by the Russell 3000 Index. These headlines are not offered to explain market returns. Instead, they serve as a reminder that investors should view daily events from a long-term perspective and avoid making investment decisions based solely on the news.

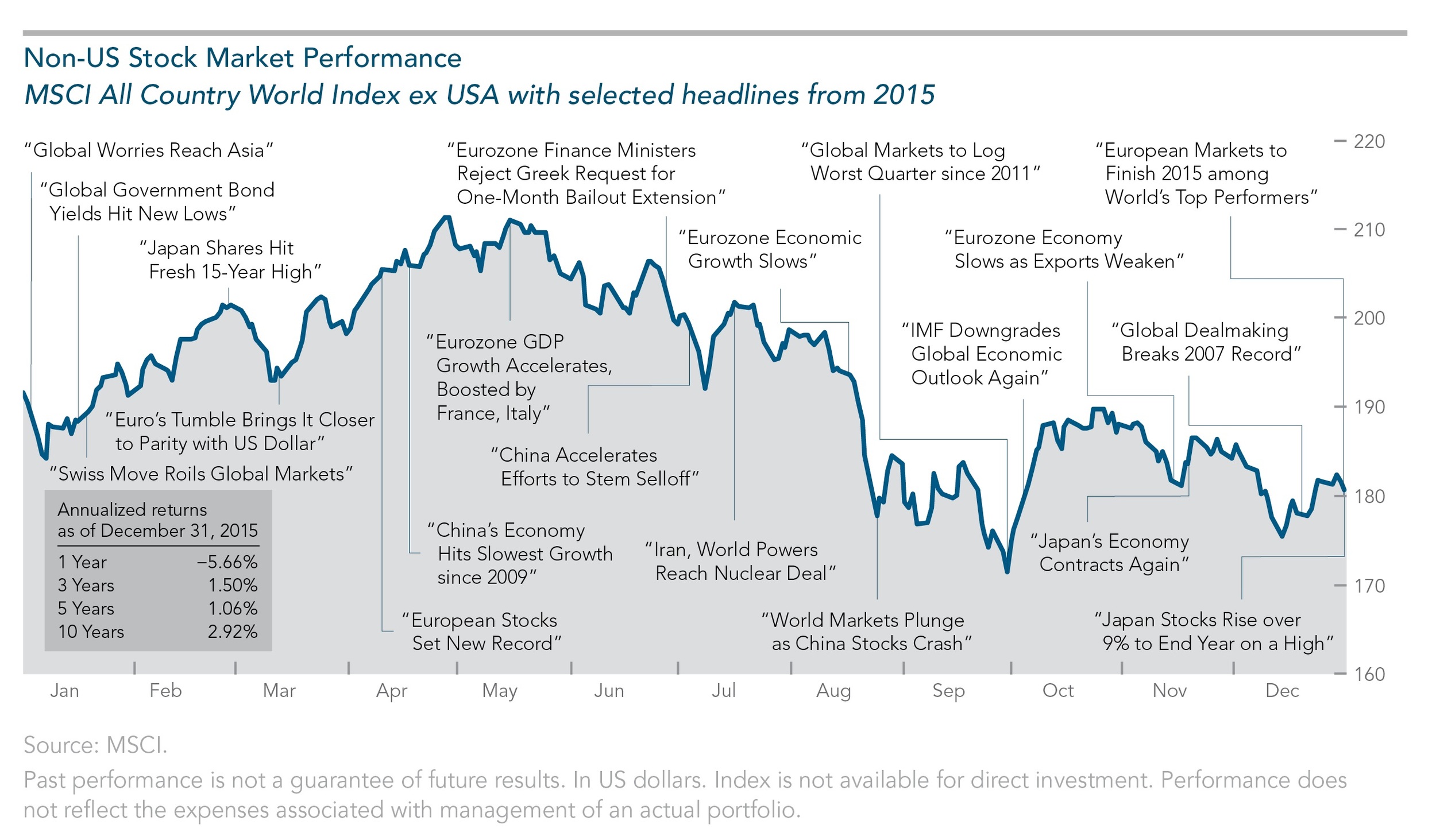

The chart below offers a snapshot of non-US stock market performance (developed and emerging markets), measured by the MSCI All Country World ex USA Index. The headlines should not be viewed as determinants of the market’s direction but as examples of events that may have tested investor discipline during the year.

Global Backdrop

US Economy

The US economy grew modestly during 2015. Gross domestic product (GDP) increased only 0.6% in Q1 before improving to 3.9% in Q2 (year over year). Growth slowed to 2.0% in Q3, matching the average annualized growth for the past six years. Q4 GDP growth was forecasted to decline to 1.0% and GDP growth for all of 2015 to average 2.5%.

Positive economic signs in 2015 included lower unemployment, which fell from 5.7% in January to 5.0% in the last three months of the year—the lowest rate since 2008. Overall, the economy added 2.7 million jobs, capping the second-best annual gain since 1999. December wages were up 2.5% (year over year), which marked one of the best gains of the current expansion, although still below the 6.33% annual average. Inflation (personal consumption expenditures index) remained low. November’s 0.5% rate (year over year) marked the 43rd straight month of annualized inflation below the Fed’s 2% target rate. US housing activity remained solid with price growth, as measured by the S&P/Case-Shiller Home Price Index, rising 5.2% (year over year) through October. New home sales increased 14.5% through November. Consumer confidence also improved, with the University of Michigan’s Index of Consumer Sentiment averaging 92.9 in 2015—the highest since 2004. Consumer spending, which accounts for more than two-thirds of US economic activity, grew 3.0% in Q3.

Negative economic indicators included declining US factory activity. In December, the Institute for Supply Management’s (ISM) index fell to 48.2 from 48.6 in November, which was the weakest reading since the final month of the recession in June 2009. (Readings below 50 indicate contraction.) Corporate profits declined in Q1 and Q3 by 5.8% and 1.6%, respectively, and profits at S&P 500 companies were projected to fall by 3.6% in Q4.

Global Economy

In 2015, economic growth was the weakest since the financial crisis. In December, the Organization for Economic Cooperation and Development (OECD) revised its 2015 world growth estimate downward to 2.9%—well below the historical average of 3.6% per year.

Eurozone GDP growth increased 0.5% in Q1, which was the strongest quarterly rate since its regional recovery began in early 2013. But the pace slowed to 0.4% in Q2 and to 0.3% in Q3. The slowdown came in spite of improved consumer spending sparked by lower energy prices and the European Central Bank’s (ECB) quantitative easing efforts. A decline in the euro’s value boosted exports and contributed to an improved current account surplus (3.7% of GDP) in 2015. Japan’s economy showed signs of improvement early in 2015 by posting a 3.9% GDP growth rate in Q1. Growth in Q2 reversed with a –0.7% rate before rebounding to 1% in Q3.

China, the world’s second largest economy, showed signs of a slowdown during 2015, with Q1 and Q2 growth reported at 7% and Q3 growth falling to 6.9%, which was less than half the growth rate in 2010. The Chinese government later revised its growth target to 6.5%, reflecting the weakest growth in 25 years.

After several years of robust growth, emerging market nations began to feel the effects of China’s slowdown, persistently weak global commodity prices, and the prospect of higher US interest rates. In Q4, the International Monetary Fund (IMF) cut its 2015 growth estimate for emerging markets to 4%, which marked the fifth consecutive year of declining growth.

Oil Market Decline

The world oil market continued its dramatic slide. After falling more than 50% in 2014, oil declined another 30% to end 2015 at $37.04 a barrel for West Texas intermediate crude, marking the largest two-year price drop on record. Factors affecting the price decline include: (1) excess supply spurred in part by higher production in North America, Middle East, and Russia, (2) slack demand due to slowing global growth, especially in the emerging markets, and (3) OPEC’s waning ability to influence market prices by adjusting its production. While cheap oil was a boon to consumers in developed economies, the steep price decline brought uncertainty to financial markets and industry sectors as firms curtailed spending and canceled projects, and oil-exporting countries collected lower tax revenues and struggled with the effects of a weaker currency.

Diverging Paths for Central Banks

The divergence in actions by the major central banks in 2015 marked the first time since the euro’s launch that the Fed, ECB, and Bank of England have been compelled to strike different monetary paths as a result of diverging economies. In the late 1990s, the booming global economy led the central banks to apply rate hikes, while the 2001–2003 market decline brought similarly timed rate cuts.

In September, the Fed postponed raising interest rates, citing concerns with the economy, inflation, and worldwide market volatility. The central bank raised its benchmark rate by a quarter point in December—its first rate hike since 2006—and stated that it would continue on a gradual course of monetary tightening as long as inflation and economic growth allowed. The impact on the US financial markets was negligible, as rates had already begun to increase in anticipation of the move. Even as the US central bank began monetary tightening, most banking authorities across the globe were taking measures to ease their country’s monetary policy in response to signs of an economic slowdown. The ECB implemented a major stimulus program throughout the year, and in December announced new quantitative easing measures along with Japan. More than 40 central banks across the globe eased monetary policy in 2015.

China’s Rising Influence

Markets closely followed the news about China’s declining economic growth and the severe downturn over the summer, when the Chinese equity market declined more than 40% from its peak. Attempts by the Chinese authorities to support stock prices and the Bank of China’s surprise devaluation of the yuan raised questions about China’s impact on the economies of trading partners. The events also pointed to the stresses the government faces in implementing additional free-market reforms and transitioning its economic model from heavy industry and exports to one based more on consumer spending.

2015 Investment Overview

Market Summary

In the US equity markets, most major indices logged negative performance, despite a strong rebound during Q4. For the year, the S&P 500 Index returned 1.38%; the Russell 3000 Index 0.48%; and the Russell 2000 Index ‒4.41%.

US market volatility, measured by the Chicago Board Options Exchange Market Volatility Index (VIX), declined steadily for the first half of 2015, but jumped to its highest level in six years in late August, following the US market decline. During Q4, the index dropped then rose again to close slightly higher for the year.

Non-US developed stock markets experienced mixed performance across almost all major indices (returns in USD, net dividends). The MSCI World ex USA Index, a benchmark for large cap stocks in developed markets outside the US, returned ‒3.04%. Small cap and value stock returns were mixed: The MSCI World ex USA Small Cap Index returned 5.46% and MSCI World ex USA Value Index returned ‒7.68%. The MSCI World ex USA Growth Index was positive at 1.65%. Emerging markets were among the worst global performers: The MSCI Emerging Markets Index returned ‒14.92%; the small cap subindex returned ‒6.85%; the value subindex returned ‒18.57%.

Among the equity markets tracked by MSCI, nearly half of the countries in the non-US developed markets index had negative total returns (in USD) and the range of returns was broad. The top three return countries were Denmark (23.43%), Ireland (16.49%), and Belgium (12.10%). Countries with the lowest returns were Canada (‒24.16%), Singapore (‒17.71%), and Spain (‒15.64%).

In emerging markets, 21 of 23 countries tracked by MSCI logged negative total returns (in USD) and the dispersion of returns was broader than in the developed countries. Hungary (36.31%), Russia (4.21%), and India (‒6.12%) were the top-performing countries in the index. The lowest returns in the index came from Greece (‒61.33%), Colombia (‒41.80%), and Brazil (‒41.37%).

Returns of major fixed income indices were slightly positive. One-year US Treasury notes returned 0.15%, Barclays US Government US Bond Index 0.86%, Citigroup World Government Bond Index (1‒5 years, USD hedged) 1.00%, and Barclays US TIPS index returned ‒1.44%. The Barclays Global Aggregate Corporate Bond Index 1–5 Years (hedged to USD) returned 1.21%.

US and global real estate securities had mixed performance: The Dow Jones US Select REIT Index returned 4.48%, and the S&P Global ex US REIT Index returned ‒3.54%. Commodities were negative for the fifth year in a row, with the Bloomberg Commodity Total Return Index returning ‒24.66%. Among the composite indices, petroleum returned ‒39.42% and industrial metals ‒26.88%. Among the single commodity indices, Brent crude (‒45.57%) and West Texas intermediate crude (‒44.35%) were the worst performers. Natural gas returned ‒39.95%. Gold was down for the third year in a row at ‒10.88%; silver prices returned ‒12.72%. Cotton was the only commodity in the index to post a positive return (2.97%).

Currency Impact

The US dollar rose against most major currencies, including the euro, pound, and yen. The dollar’s strength had a negative impact on returns for US investors with holdings in unhedged non-US assets. For example, in 2015, the dollar’s rise relative to the euro hurt the returns of US investors in European markets. The MSCI Europe Index (net dividends) returned 8.22% in euro but ‒2.84% in US dollars. This was the case in other regions where the dollar outperformed local currencies. Examples: The MSCI United Kingdom Index (net dividends) returned ‒2.21% in pounds and ‒7.56% in USD. The MSCI Australia Index returned 1.29% in Australian dollars but ‒9.95% in USD.

Performance of Size and Value Premiums

Based on the respective total returns of the Russell indices(1) within the size dimension, US small cap stocks underperformed US large cap stocks by ‒5.33% (‒4.41% vs. 0.92%). Within the relative price dimension, US value underperformed US growth by ‒9.22% (‒4.13% vs. 5.09%). Among US small cap stocks, small value underperformed small growth by ‒6.09% (‒7.47% vs. ‒1.38%); among US large cap stocks, large value underperformed large growth by ‒9.49% (‒3.83% vs. 5.67%).

As in most years, diverging performance of various subindices in 2015 underscores the fact that the premium within a particular dimension (e.g., size or value) does not always move in the same direction across the global markets. For example, although the size premium was negative in the US, it was positive in both the developed non-US and emerging markets for the year. The MSCI World ex USA Small Cap Index outperformed the MSCI World ex USA Index by 8.50% (all returns in USD, net dividends). The MSCI Emerging Markets Small Cap Index outperformed the MSCI Emerging Markets Index by 8.07%. Value premiums outside the US were generally negative. The MSCI World ex USA Value Index underperformed its growth counterpart by ‒9.33%; the MSCI Emerging Markets Value Index underperformed the MSCI Emerging Markets Growth Index by ‒7.24%.

Annual underperformance of the size and value premiums is not unusual from a historical standpoint. Although small cap and value stocks have offered higher expected long-term returns relative to their large cap and growth counterparts, these return premiums do not appear each year.1 For example, since 1979, US small caps have outperformed large caps in 19 of the 37 calendar years—or 51% of the time. Results are similar for the relative price dimension. Since 1979, US value has outperformed growth in 20 of 37 calendar years—or 54% of the time. Small cap value has outperformed small cap growth in 57% of the calendar years.

History also has produced multiyear periods in which US small cap and value stocks did not outperform large caps and growth. The most recent example is three-year underperformance of small cap value vs. small cap growth (2013‒2015). Small value has also underperformed in three straight years (2009‒2011 and 1989‒1991). Other multiyear examples include small caps underperforming large caps (1984‒1987 and 1994‒1998) and value underperforming growth (1989‒1991 and 2009‒2011). Yet, despite even extended negative-premium periods, small cap and value stocks have outperformed their counterparts over time, and when the premiums reversed, they often did so strongly and for multiple years.

(1) US small cap is represented by the Russell 2000 Index; US large cap is the Russell 1000 Index; US value (marketwide) is the Russell 3000 Value Index; and US growth (marketwide) is the Russell 3000 Growth Index. US large value is the Russell 1000 Value Index; US large growth is the Russell 1000 Growth Index. Russell data © Russell Investment Group 1995–2016, all rights reserved.

Russell data © Russell Investment Group 1995–2016, all rights reserved. Dow Jones data provided by Dow Jones Indexes. MSCI data © MSCI 2016, all rights reserved. S&P data provided by Standard & Poor’s Index Services Group. The BofA Merrill Lynch Indices are used with permission; © 2016 Merrill Lynch, Pierce, Fenner & Smith Inc.; all rights reserved. Citigroup bond indices © 2016 by Citigroup. Barclays data provided by Barclays Bank PLC. Indices are not available for direct investment; their performance does not reflect the expenses associated with the management of an actual portfolio.

Past performance is no guarantee of future results. This information is provided for educational purposes only and should not be considered investment advice or a solicitation to buy or sell securities.

Investing risks include loss of principal and fluctuating value. Small cap securities are subject to greater volatility than those in other asset categories. International investing involves special risks such as currency fluctuation and political instability. Investing in emerging markets may accentuate these risks. Sector-specific investments can also increase these risks.

Fixed income securities are subject to increased loss of principal during periods of rising interest rates. Fixed income investments are subject to various other risks, including changes in credit quality, liquidity, prepayments, and other factors. REIT risks include changes in real estate values and property taxes, interest rates, cash flow of underlying real estate assets, supply and demand, and the management skill and creditworthiness of the issuer.

Dimensional Fund Advisors LP is an investment advisor registered with the Securities and Exchange Commission.