Exhibit 1

The Wall Street Journal published an article this week titled, The Dying Business of Picking Stocks. In the piece, there are some startling statistics that demonstrate the massive shift away from high cost active fund management to low cost passive approaches. Some that caught my eye:

- Over the three years ended Aug. 31, investors added nearly $1.3 trillion to passive mutual funds and their brethren—passive exchange-traded funds—while draining more than a quarter trillion from active funds, according to Morningstar Inc.

- Hedge funds, which bet on and against stocks and markets world-wide and generally have higher fees than mutual funds, haven’t outperformed the U.S. stock market as a group since 2008.

- Although 66% of mutual-fund and exchange-traded-fund assets are still actively invested, Morningstar says, those numbers are down from 84% 10 years ago and are shrinking fast.

- Over the decade ended June 30, between 71% and 93% of active U.S. stock mutual funds, depending on the type, have either closed or underperformed the index funds they are trying to beat, according to Morningstar.

- Public pension plans had 60% of their U.S. stock allocations in index funds in 2015, up from 38% in 2012, according to research firm Greenwich Associates. At endowments and foundations, the index-fund share rose to 63% from 40% in that time period.

The world has changed dramatically from my early days at Fidelity Investments when the Magellan fund was still basking in the glow from the Peter Lynch years where he more than doubled the return of the S&P 500 index from 1977 to 1990. Investors literally would stand in line waiting to invest their money with us.

Fidelity manages hundreds of funds, but the small minority of managers, like Lynch, that were able to beat the market for a while were marketed so effectively that they became the largest fund company in the world. Interestingly, Fidelity’s own 500 Index fund has almost surpassed their largest actively managed fund, Contrafund.

You may have seen Contrafund on television recently as Fido has been advertising customer letters written to the manager, Will Danoff. I guess you can’t blame them for trying to rekindle some of the Lynch years’ magic for their current statistical oddity, er, I mean star manager.

Academics have consistently shown that the vast majority of managers don’t beat the market. However, there will likely be the occasional outlier, like Lynch or Danoff, that will come along from time to time. There is no doubting their success, but due to their rarity, it is a fool’s errand to try and figure out who is likely to be the next longshot winner. You could chase the performance by investing in a fund like Contrafund, but how much longer will Danoff be there considering he took it over in 1991?

One of the arguments made by critics of passive investing (usually those in the business of active stock picking) is that with increasing index investing, active managers can more easily exploit inefficiencies in markets. The first time I heard this argument was probably 10 years or so ago, by Fidelity Chief Executive, Abigal Johnson at a conference I attended. So far, the evidence hasn’t favored that point of view.

In fact, as you can see in Exhibit 2, only about a third of active managers have beaten their benchmarks in the last decade or so. Even when you take the winners and look at them in subsequent periods, only about a third of them continue outperforming.

Exhibit 2

What the long term evidence has shown, is that markets do a good job of fairly pricing stocks. Furthermore, if you are willing to take on the additional volatility, some types of stocks have demonstrated persistent out-performance. I have shared some of this information before in the February 19, 2016 Accountable Update.

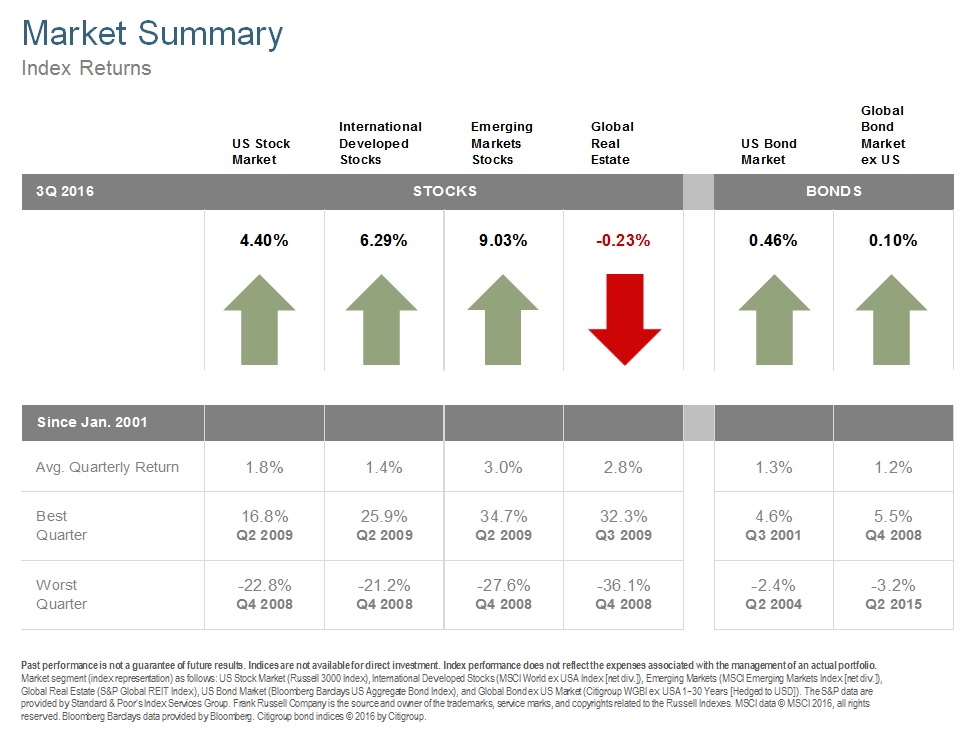

If you missed it, the Cliff’s Notes version is that small companies have consistently outperformed large companies, value has beaten growth, and companies with high profits have returned more than those with less. These premiums have in some cases been observed for close to a century, and in markets both foreign and domestic (see Exhibit 1), albeit they don't occur every year or even every decade, as seen in Exhibit 3.

Exhibit 3

All of this is to say that the WSJ article may be correct in pointing out that investors have become much more savvy in their choice of investment approach. But the death of the “business of stock picking” may have been exaggerated. The evidence points us not to an untimely demise, just a smarter way to go about “picking”. If you have questions about how your picks are working out, get in touch.